Warden Capital Q1 2024 letter part 2

More commentary on the REIT & CRE markets

Well what a difference a hot CPI report makes… the 10 year is up over ~4.6% today and REITs have been down broadly the last few weeks. As I already covered in part 1 - the REIT market is too focused on inflation.

However given the market’s obsession over inflation, I’ll do a little update here. If you don’t care, skip down to the sector specific information below.

And as always, nothing here is investment advice! Do your own diligence & research, consult with a financial advisor. Please read our general disclaimer here

For what it’s worth - I’m still not fully convinced inflation is stuck. Some other data points support a continued downward trend in inflation. First and most importantly, wage growth has continued to decline. The latest Indeed figures came out, with March now coming in at pre-covid levels of wage growth.

This is in my view, a pretty big deal!

Even more interesting to me is that the Atlanta Fed’s wage tracking data has resumed its decline, which supports the Indeed data as being a leading indicator.

The Atlanta fed wage data is down to 4.7% YoY, and has declined a whopping 50 bps since December.

This is frankly almost a worrisome rate of decline, however the flatline in fall of 2023 and otherwise healthy labor data makes me feel fairly sanguine for now. It looks like at current pace the Fed data could show us at pre-covid wage growth levels by the end of this year. And interestingly most people don’t seem to realize this, I still see loads of commentators and ‘experts’ talking about nominal wage growth being 6-7%.

Furthermore it looks like the March PCE (the Fed’s main focus) should be a good bit softer than CPI as we had a softer PPI report which is a key feeder into the PCE data. Also more broadly basically all of the excess inflation in the March CPI came from housing (highly lagged as I have discussed), and auto insurance & repair, which is also arguably a lagged reflection of the huge spike we have had in used vehicle prices.1

All that said, I don’t have a terribly strong opinion as to whether inflation is turning sticky or will continue falling2. But I do think a higher inflation environment is bullish for CRE prices as it drives higher increases in construction costs & property incomes. Again look at what happened to property prices in the 70s and 80s - absolutely huge annual increases.

The big risks in my view are demand destruction aka recession, or a rapid change in financing costs (what we just saw). If we did see another spike in interest rates, you could see CRE prices fall another 5 to even 10%.3 I don’t think this will happen, as I believe it would require inflation heating back up a good bit which I don’t see evidence of yet. But I could be wrong here!4 Luckily for us, there are already many REITs trading at 10%+ discounts to private market values, so we are insulated from long term losses should prices in fact decline further.

My view is it is too difficult to truly know what will happen here, and the best you can do is focus on buying quality assets with good demand profiles at attractive prices & below replacement cost. Long term this will work out, as long term it is supply (and therefore construction costs) and demand which drive CRE pricing, not financing costs.

Onward to the sector specific commentary.

Office:

While we are being negative, lets start off with the weakest office class, office. At the margin if inflation & rates get stuck I think the downside risk is higher for weak office properties (which is a lot of the asset class). This is because with weak demand you can’t actually pass through the cost increases from inflation, and with no need for new construction replacement cost no longer has any bearing on market prices and values.

And demand is weak pretty much everywhere. As I have said before, I think you have the foundation for a recovery over the next few years in NYC/Boston, the top sunbelt markets, and even SF/Seattle if AI growth really does take off. Everywhere else is basically un-investable until prices fall further.

I have covered NYC extensively here so don’t need to spend too much time on it (see prior posts here, here and here), but do want to check in. Vacancy ticked back up a little bit in Q1, so its probably premature to say the market is recovering but at least it seems to have stopped its fall or is close to doing so, which is positive.

Certain submarkets, like Park Ave, are actually starting to get tight! The bifurcation in quality/location preference is real. Here is a nice chart from VNO’s annual letter that illustrates the stark divide in the market today.

RTO has crept a bit higher, but is moving very slowly and we are probably close to a new normal. VNO’s portfolio utilization rates are around 65%, vs 80% pre-pandemic. So about 81% of pre-pandemic levels. This gels with Placer.AI’s data of around 80% as well. This level is high enough to minimize demand destruction for firms that are still in office - if its basically just Fridays that are WFH there isn’t a realistic way to shrink your footprint.

Similar to NYC several major sunbelt markets have stopped their decline. DFW for example seems to have leveled off and appears to be on the slow road to recovery.

With the incipient AI boom the tech markets appear to have a potential ladder out of this mess, and could conceivably actually be the first to recover. This subject deserves a deeper dive, but at a high level in terms of actual employment the AI sector is basically nothing (Open AI only has ~1,200 employees!), and if this really is an internet level technology shift then that number could become absolutely massive.

And you are already starting to see what may be the start of a recovery in Silicon Valley, without the benefit of much AI hiring. Here is the San Jose / Silicon valley availability rate. Q1 of 24 saw a huge downtick of 0.8% in terms of vacancy, and even more in class A.

It is important to note this recovery appears to be driven more by removal of sublease space instead of leasing, but from the point of view of a landlord both are good.

So that’s the ‘good news’ if you can call it that, in the office sector. The knife seems to have stopped falling, at least in a handful of markets.

That said, I am still very bearish on weaker office properties in weak markets - I have seen some private market sales in secondary markets which I think will work out poorly for the buyer. I compare public market pricing to public, but I also evaluate whether private market pricing feels attractive.5 I think most asset classes on the private side feel decent to good right now, but the one area that I think feels markedly unattractive is B/C office in weak markets.

NLOP is an interesting case here - this one has been going around fintwit. NLOP and others have been able to sell what are pretty bad assets IMO for surprisingly low cap rates / high prices. I’m not going to argue with the private market prices - it does appear that there is a decent sized spread between those prices and NLOP’s implied price today. However I do not like investing in a spread based on what I view as unsustainable or unattractive private market pricing - this is a dangerous game as if private market prices do indeed decline further you are left holding the bag. And in this case I believe those weak office asset prices have a good chance of declining further.

I’d much rather buy a smaller discount but in something where I think the underlying private values are likely to appreciate over the next several years.

Industrial:

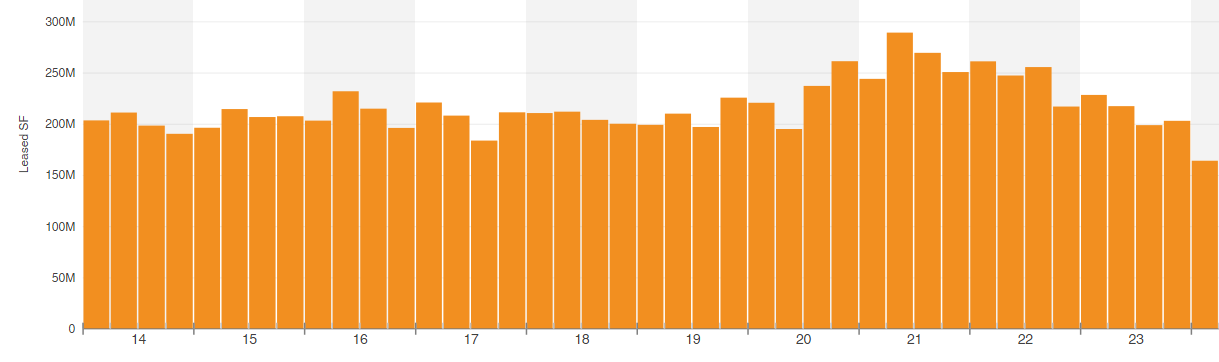

The industrial market continued to cool off in Q1, and certain markets are showing outright weakness. Most notably leasing posted a meaningful drop across the country, which combined with the significant new supply has continued to push up vacancy rates.

This can be seen in the national Costar leasing data, here.

Source: Costar market data

National industrial giant Prologis also noted this slowdown in their Q1 earnings, reducing their full year occupancy forecast to 96.25% at the midpoint, which would be down ~120 bps from 2023. PLD called out previously red hot Southern California as being particularly weak, and noted it was responsible for half of the total nominal dollar guidance reduction (they also reduced NOI growth guidance, driven in large part by lower occupancy)6.

But PLD remains fairly bullish on dynamics in 25 and 26 due to falling supply.

I agree with PLD here. Starts have been impacted by the rise in interest rates, and I expect them to stay weak until pricing recovers via lower cap rates or further additional rent growth. This means when industrial demand reverts back to its pre-covid levels (which PLD is guesstimating happens in 2025), we will start to see vacancy rates decline again and landlords pick up more pricing power. But if leasing stays soft for a few more quarters things are going to get a bit worse first before improving in 25.

Still the boom times are definitely over and I would expect a more normalized performance going forward even in good years. That said for an off year the industrial market remains decently healthy today relative to its historical performance. Outside of Southern California most markets are flat to slightly up in market rent growth, and national vacancy is around 8.5%, which while above the lows set pre-covid, is around where vacancy was in 2005-2007.

With the selloffs some of the industrial REITs became more interesting. To wit, we initiated a position in LXP. LXP owns a portfolio of newer bulk buildings in growth / non coastal markets. At today’s price (~$8.5/share), LXP is trading at an implied mid 7s cap rate, and only ~$65 per square feet, for a high quality portfolio that is only ~10 years old on average. $65 psf is basically just the hard cost for such a building today, with land, soft costs and carry you are $85-90 at least, and realistically these things need to sell for $100 psf+ to justify new construction.

Management claims the mark to market on its portfolio7 is around 13%. Even with almost no market rent growth that would bring LXP to an 8%+ yield in just a few years, which in my view is a very attractive yield for a portfolio of new bulk distribution assets in growth markets.8

LXP’s history is a bit of an interesting story - they used to be a net lease REIT, and 8 years ago began to transition to an industrial only REIT. They still have a handful of old office deals they are still trying to sell, but basically all the value comes from their industrial portfolio. The transition is essentially complete, but some investors may not quite realize it yet so there is some potential value overhang there which presumably would close over time.

Finally swinging into the realm of anecdata - as relates to industrial at least, it feels like the private investment market is picking up notably despite the slower fundamentals. Here is Hamid commenting on underwritten buyer returns compressing significantly.

On a personal level, I have seen what feels like a significant uptick in cold out reachs asking about buying some of our warehouses, and have heard competition for deals has picked up from other private buyers.

Given the weakness in multifamily, industrial is the last remaining ‘cool kid’ that all the lenders and capital providers want to invest in. At a high level I continue to expect industrial prices to benefit as capital that was previously allocated to other asset classes moves towards industrial.

So I feel pretty good about buying into industrial assets at a healthy discount to private market, when that private market price looks to be headed a good bit higher over the next few years barring a large recession.

Retail:

Retail continues to perform well. Sales are healthy to strong - January underperformed a bit YoY but February was strongly up at 1.5% YoY, and March blew past expectations coming in at a whopping 3.6% YoY!

This strong consumer spending has supported strong retailer leasing demand. And beneath all of this demand and spending is of course the American consumer, who is honestly in pretty good shape. As inflation slowed and wages remained elevated, real disposable income growth jumped over 4 % for much of 2023.

Government transfers have slowed some, but wage growth remains fairly strong which combined with falling inflation continues to yield solid real income growth. And its important to note that retail prices are nominal, not real, and the nominal consumer income growth is even higher (referring back to our ATL Fed wage tracker just under 5%).

Rising incomes of course help support rising spending, which is good for retail! There are a few potential clouds on the horizon as wage growth continues to slow, but nothing terribly concerning as of yet. Still - I don’t think the current retail spending growth is sustainable, and if wages and inflation both continue to slow spending should normalize as well.9

Of course the strength does not extend through the entire sector - weaker malls & centers continue to decline and die, however this actually benefits the assets which survive as that spending is redistributed across other centers.

There remains some churn as certain retailers perform better than others but this is normal. A few pieces of notable news are the Joannes bankruptcy, which was quite positive in that thus far they are not planning on closing any stores, and Family Dollar / Dollar Tree planning to close around 1,000 stores. Interestingly though Dollar General is still very much in growth mode, so this may be more of a company level issue.10 Department stores also continue to struggle, with Macys announcing another 150 store closures.

Generally I find it a bit interesting that many of the retailers who were still expanding in the 2015-2020 period are now struggling and closing stores. Big Lots, Dollar Tree, & many of the pharmacies seemed like the only game in town for retail leasing for years, and now it looks like they all over expanded. Offhand really only TJX seems to have managed that growth well.11

In our own portfolio, MAC remains the star of the show here. Notably the old CEO retired and they brought in Jackson Hsieh, the former CEO of Spirit Realty. Jackson is well regarded on the street and I view the change positively.

Leasing remains really strong, with 2023 coming in at 4.2 million square feet, a record year for MAC. This strong leasing translates into a really strong signed not opened pipeline of $64 million, which will mostly hit in 2024 and 2025.

And despite some macro uncertainty, retailers continue to lease new space.

Mac did an impressive 4.5% same store NOI growth in 2023, and is well positioned for a strong 2024. Mac is only guiding to ~2.75% NOI growth for 24 - they expect some further headwinds from expense inflation & some temporary decline as space turns over, but I also suspect they are being conservative with this number and they are likely closer to 4% growth.12 Mac is exposed to the struggle of department stores like Macy’s, but they have had great success releasing department store boxes and given the low rents the department stores pay the process is often quite accretive despite some large up front capex investments.

While MAC has rallied a good bit, it still trades at what I view as a very attractive NOI yield of ~7.8%. Combined with its likely income growth of 3%+ over the next several years, and there is just nothing else with such an attractive combination of yield, stability and growth in the REIT space.

Compare this to investor darling industrial. Once you mark the industrial REIT rents to market the implied yield is in the low 6s (varies by REIT of course). So you have to believe industrials will grow income at ~5% for a decade, after marking up rent to match an investment in MAC.13 Given the commodity nature of warehouses I find this extremely unlikely.

Hotels:

I have written a good bit on hotels recently, (article here), so I’ll make this section shorter but will provide a brief update. The hotel sector as a whole had a fairly strong end to 2023, and our major investment, Park, had a very strong end to the year.

Overall the hotel market continues its normalization, and leisure remains a bit soft off its covid highs, while business and in particular group travel have continued to recover strongly.

The one fly in the ointment here is that operating expense growth has been fairly high as well, so the strong revpar growth has not translated into outsized NOI growth (although it has still been respectable!).

I expect tax and insurance growth to level off14, and labor costs to slow a bit as well, so this pressure should moderate somewhat in the next few years.

Park specifically has had a good Q4, with 4.1% revpar growth, about in line with my expectations. Most notably Park has had a really strong start to 2024, with a whopping 13.4% YoY revpar growth in January and ~8% in February.15 This is driven in large part by strong recovery in Park’s urban, and in particular group driven markets.

This strong group pace of 13% YoY for 2024 should should help Park generate robust revpar growth relative to other hotel REITs, thanks to its very group oriented portfolio of large assets with significant amounts of meeting space.

Overall given the strength of the US economy & consumer I would expect hotel demand to be pretty healthy in 2024. The real question for NOI growth will be if expense growth levels off as well. Generally though given the favorable limited supply backdrop, this combination of strong demand growth and minimal supply should continue to provide a really nice tailwind for hotel owners over the next few years.

Storage:

We’ll wrap things up with storage, a sector near and dear to my heart on the private side, although we don’t own any of the storage REITs at the moment. In general the storage market is very weak right now, with new rental rates in particular down massively in many markets (national averages over a 10% decline per Green St, which feels about right from the markets I follow), including most of our covid boom poster children.

REIT results have not been quite as bad as their big coastal markets like LA & NYC have held up better, and they have also been able to offset much of the street rate weakness with strong rate hikes on existing customers. Public Storage’s results illustrate this pretty nicely, as PS was able to raise revenues over 4% on the year despite declining occupancy!

Also note the sunbelt & FL markets at 2-3%+ occupancy loss from 22 to 23, vs coastal ~1-1.5%.

If street rates stay this low for another year though, the lower street rates will really begin to impact REIT results. However if demand recovers sufficiently the REITs may well be able to skate through without significant NOI declines.

We will see what happens here - storage is very volatile on both demand and supply given its relatively small size. Moves are a big driver of storage demand, so more home sales / apartment rentals = more storage demand. Apartment leasing has been quite strong which would be bullish for storage demand and so we will have to see what the single family sale market does this year.

Fin

I’ll leave it here for now - these letters are becoming a bit unwieldy, I may try to trim them in the future. To recap, I believe we are at or near the bottom in pricing for most asset classes, and we should see pricing rise from here driven primarily by rising income growth. I expect multi, storage and of course office to be laggards due to their weaker near term demand profiles & thus weaker income growth. Hotel and retail demand is healthy, industrial is decent, and multi demand is fairly strong but is just overwhelmed by even larger supply. Office remains very weak, although there are glimmers of life in a few markets.

We have seen lots of volatility in the REIT market as it obsesses over inflation, but I believe if you can ignore the noise and stomach the volatility the REIT market continues to be a very interesting place.

There are likely some absolute levels of premium increases here as well in fairness. Your premium is of course determined by vehicle cost, so as vehicle costs go up premiums will as well.

I lean towards the data indicating it continuing to fall in case you can’t tell. But inflation is so complex it is hard to have a high confidence opinion on the subject in my view.

And by spike I mean the 10 year going to mid 5s or higher - I’d wager that gives us another leg up in cap rates. However price declines would be offset by income growth in many asset classes, which is what gives me some confidence we are at or close to the bottom in private market prices. As even if rates go higher prices probably just bounce along the bottom for another year rather than declining much further (for assets with good demand). I think you’d need the 10 year into the 6s for meaningful further CRE price declines, or a recession.

There is a recursive game one can play thinking about higher inflation → higher rates → higher odds of recession → lower long term rates.

Not enough investors do this - it is pretty easy to calculate an NAV for a REIT and compare it against the current stock price. It is much harder to have an informed opinion about private market pricing as it requires deep asset class, geographic and economic analysis.

So Cal is ~20% of PLD’s NOI & is their largest market by some margin, so they are heavily exposed to it for better or worse.

That is if you were able to magically increase the rents on all leases to today’s market rent.

~25% of so of the portfolio is in the Midwest which has a weaker growth profile. That said the Midwest industrial markets have actually done fairly well, albeit nowhere near as positive as the coasts.

Of course if inflation is indeed stuck then high retail spending growth could continue.

They also are situated in different markets which may explain some of the differing performance as well.

I’m sure I’m missing a few others who have also done well.

What may happen is that MAC may have a relatively weaker 2024, close to guidance, and then a very strong 2025. As much of the expense growth is probably ‘catch up’ in taxes and insurance from higher property values, which as that levels off should allow the typical 2-3% annual lease escalations to contribute to NOI growth again. The escalations combined with strong leasing could generate a 6-7% year in 2025. But it looks like MAC is well set up to average ~4% NOI growth for the next few years.

Its not quite this simple as one must also compare capex profiles. While malls have had very elevated capex recently this is likely going to fall significantly as the department store boxes are re-tenanted, and should be in line with industrial soon. Historically malls were the lowest capex asset class, before their recent bout of weakness. And if you are curious, at 5% growth for industrial and 3 % for malls, it would take 14 years for industrial to catch up. Even at 2.5% its 10 years!

These are both driven by property values, which have of course rallied significantly from covid era lows for hotels. Insurance also has been going through a large rate hike cycle, something which appears to be finally slowing down & so going forward this should normalize once costs are caught up.

They expect March to be weaker and Q1 to end up around 6-7%, which would still be great.

Excellent! Please do not trim the letters, this is gold