War Cap Year End 2023 letter

Comments on the CRE & REIT markets

I have been travelling but I am belatedly getting around to sharing my 2023 year end letter. Again as always please review my disclaimer here, nothing here is investment advice. The market (and our performance) is down a bit since YE, but I still feel fairly good about 2024. I am hopeful we are generally close to the bottom for private market values1, and should hopefully see values begin to climb over the next several years. Combined with continuing healthy discounts to private NAV at many REITs and the 3-4 year picture still looks quite attractive in my view.2

Dear investors,

I am writing to give you our year end 2023 update. We have had a phenomenal year, with YTD returns at 49.99%, far exceeding our benchmark USRT's3 return of 12.98%, and even the S&P's strong 26.29%. Since inception the contrast is even greater, at 167.84% vs 51.89% for the USRT and 76.38% for the S&P. We have outperformed the USRT every year since inception in 2020.

Performance comparison of sample $100k investment.

I dislike self promotion, but if there was ever a year to take a victory lap, this is it.

This final quarter in particular has been very strong, with gains across the entirety of the portfolio. For the year, our strongest performer was VNO. VNO was up 34.33% on the year, which is very good, but I doubled down on the stock when it traded down into the mid teens, and those investments are up ~100%. This is an excellent example of the value good active management can add, and was enabled by my strong conviction in the value of the underlying portfolio. Other strong performers this year were Park Hotels, up 32.93% (more when you factor in their large year end dividend), and Macerich, up 38.01%. Not every stock we owned was so good, but these were our 3 largest positions.

Overall – despite the rapidity of the recent rise in prices, nothing in our portfolio is as of yet above or even at NAV. Further generally I think at this point the trend will be for NAVs to increase as private sector values in many asset classes begin to claw their way back. So, despite the rapid rise in prices, I still feel pretty good about our portfolio. However that value gap is far smaller than it was earlier this year, and returns should be more moderate going forward.

The strong performance of our investments was driven both by solid operating performance of the underlying firms, and also an overall rally in the REIT market (which obviously we outperformed).

The REIT rally was driven by the continued moderation of inflation data & treasury rates. I discussed this extensively in my Q3 letter – at that time I was puzzled by the continued spike in treasury rates despite very favorable inflation data. The market seems to have finally got the memo several months later, and at the time of this writing the 10 year rate is around 3.95%4, a whopping nearly 100 basis points below where it was at the writing of my Q3 letter. Amusingly enough though the rate is actually just about where it was when the year began.

Given the softness in apartment rental data & used cars, I am hopeful we should have a continued glide path towards lower inflation rates at least in the first 6 months of 2024. The fed has acknowledged this and is now guiding towards a few rate cuts in 2024. Wage growth has continued to decline, although remains slightly above pre-Covid levels. Personally I am not terribly worried about slightly above trend wage growth – if the economy can deliver moderate or even goods disinflation while wages are growing strongly, is that not the best possible outcome for the country? Much better in my view to have strong wage growth, especially for lower income people, than for the country to have ultra-low interest rates which only really benefits a few very leverage sensitive investors.

That said, wage growth may well continue its decline back towards pre-covid levels. Ultimately, the economy isn’t all that different today than it was in 2019, so it would not shock me that as normalization plays out that our growth looks broadly similar to how it did back then (with a few notable exceptions).5

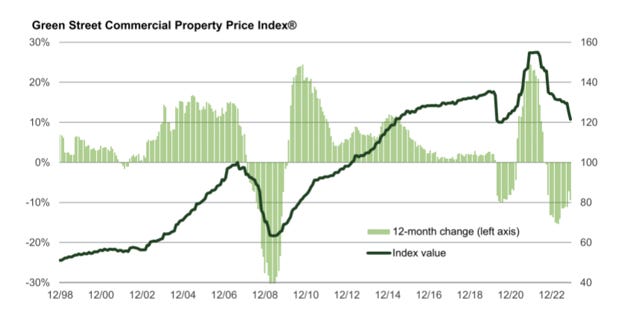

If the decline in rates continues, my assertion that real estate values are not terribly sensitive to rates over the medium & long term may well never be fully tested. The market continues to treat commercial real estate as purely a financial asset that is very rate sensitive, just like long dated bonds. As I have said time and again, this is not the case, and the long-term price drivers are the forces of supply (governed by construction costs and zoning restrictions) and demand (the drivers here vary by asset class). Obviously though in the short run a sharp spike in rates can have significant impact, as we just saw.

The rate hikes, as we all know, have driven significant value reductions in CRE across asset classes in the last year and a half, so much so that prices for most asset classes are at or below their 2014 levels! The only classes which are much higher are industrial, storage, and mobile homes.

The issue, and opportunity, here is that the cost to build a new building is significantly higher today than it was in 2015. Take apartments – costs are up ~30% since just precovid, and more like ~70% or higher since 2015. Now – prices vary significantly across markets, and the major urban market’s underperformance is pulling these averages down somewhat. For example multi prices in most sunbelt markets are not at 2015 levels – they are closer to 2019 levels (or even higher).

Setting aside the local variation, broadly speaking what this means is we need to see fairly significant price appreciation in many asset classes to justify new construction. This force should provide a strong tailwind to value appreciation over the next several years. I do not know if this will take 2 years or 5 years, but I am confident it will happen.

As I alluded to above – this supply driven pressure gives me confidence that NAVs will broadly begin to increase from here. Not every asset class, and not every market, but I would wager we are close to the bottom in terms of private market pricing, if not there already.

Of course if we have a true recession we would likely see further declines in private market values, but at this point, I just don’t see a big one coming soon (famous last words!). It is worth noting that at this point, many sectors of the economy, and also of the commercial real estate market, have essentially just gone through or are in the middle of a downturn! This means there just isn’t that much fat out there for the cutting.

On the broader economy side, we either just lived through or are in the middle of a downturn in the following (not exhaustive!) list of sectors: Travel, retail, tech, energy (remember when crude prices went negative in 2020…), financials (we did have a bit of a banking crisis in the spring), trucking, & biotech. Really the only sectors that haven’t been too badly hit seem to be manufacturing & construction. I don’t have a good read on the former, but the latter seems set for a slowdown in 2024 as the decline in commercial development starts finally begins to ripple through the system. That said strong manufacturing construction may well end up offsetting much of the decline there.

In real estate itself just about every sector has either just been through or is now going through a downturn, with the exception of industrial & single family6.

So it is really hard for me to see another broad recession coming when we basically just lived through one! The difference here is that this downturn was spread out – the ‘rolling recession’ many people were referring to really does seem to be the most apt way to describe what has occurred.

The other tail risk is a reignition of inflation. As I noted before if I had to bet, I would wager we are indeed done with high inflation, and that we should be in a 2-3% range moving forward (but my probability distribution has a decent sized chance of inflation picking up again – I think it's very hard to predict). All the same structural factors keeping inflation below that range pre-covid are basically still in place, so I don’t see why it should all of a sudden jump massively (after the covid bullwhip normalizes that is). If inflation runs a bit hotter than 2010-2019 (which I suspect it will) it looks like it will do so on the back of healthy wage growth, which again to me seems like a good thing.

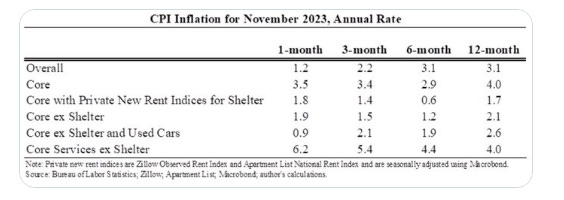

The other item giving me some comfort on inflation for at least the next ~12-18 months is the impact of housing. As I have mentioned in my prior letters – housing is a huge share of inflation data (~1/3 of CPI and ~18% of core PCE), and the way the government estimates housing cost inflation is very lagged. If you substitute in new rental data inflation over the last 12 months has actually been below 2% by a healthy margin, and over 6 months it is under 1%!

Chart is from economist Jason Furman. Again worth a follow on Twitter!7 I would normally share PCE here but he hasn’t posted the latest PCE data (which was broadly very good) – the PCE with private new rent though would be a bit higher than the CPI, but still well below 2% on a 6 month basis (which is when inflation really started to slow down)

These low housing inflation figures are because many markets (particularly those in the sunbelt) are seeing YoY rental rate declines. More on this in the apartment section, but broadly speaking given the supply pressures multifamily is going to face in 2024 (which is to say record deliveries), the housing inflation data should continue to decline, which will in turn put downward pressure on the headline rates.

But inflation is very difficult to forecast, and in my view what inflation does will not significantly impact our medium to longer term performance. So I am not terribly worried about higher inflation.

This is because private cap rates have already been marked up to rates that are more consistent with ‘higher for longer’. Any scenario with sustained high inflation is going to generate healthy NOI growth, which will in turn lead to value appreciation (underpinned by replacement costs rising even higher). Now in the short run if inflation picks up I would not be shocked if the REIT market freaks out, given how it has behaved thus far. But private market values I don’t think would move too much further in a higher for longer scenario, and eventually will start to rise driven by strong income growth. So this does present some short term ‘risk’ to our portfolio, but I don’t think it would actually impair values over the medium term and thus I don’t worry about it too much. I care about the risk of permanent capital impairment, not short term volatility.

But that is enough macro discussion for this letter, onward to asset class specific commentary.

Retail

We will start with retail. The story here is pretty similar to where we stood in Q3. Consumer spending remains very strong – and retail leasing thus far has also been at historically high levels.

Of course not every single retailer is performing well. Notable weak performers are home goods & home improvement retailers, who are suffering from the slowdown in home sales, sporting good sports (likely a covid normalization bullwhip), and electronics retailers. Luxury goods, which aren’t broken out in the census data, are also beginning to soften a bit. It is also important to understand that department stores continue to struggle (they are buried in the General Merchandise category).

Still – overall the retail market continues to perform well, buoyed by minimal new supply. The demand side appears to have solid underpinnings as well, with inflation adjusted wage growth finally re-emerging due to continued healthy nominal wage growth with lower inflation.

As it relates to our portfolio in particular, Macerich has continued to have a very good year. They have had 5% NOI growth YTD, and look set for continued strong growth in 2024 and 2025. Mac’s signed not opened (SNO) & under negotiation leasing pipeline has grown to a whopping $75 million in incremental rent growth.

That is nearly a 10% increase on current NOI. Now – MAC will also lose some tenants which will offset a bit of this growth, but it shows just how much near term income MAC is likely to see. This also doesn’t even count the typical ~3% rental escalations the existing tenants have. As Mac’s CAM structure has fixed escalations inflation chewed up a good portion of their in place rate escalations in the last few years, but as inflation has fallen these rental rate increases should begin to power further NOI growth in 2024. Net net - it wouldn’t surprise me if MAC can do 5% NOI growth in 2024 and 2025 if we can avoid a recession.

Hospitality

I covered hospitality pretty extensively in my last substack post, available here. So I won’t rehash it too much here.

I was intending to do a deep dive of Park Hotels, one of our major holdings but the stock has moved so much in the past month the current valuation, while attractive, isn’t quite as good as it once was.

Park’s valuation has obviously moved in the right direction, but its operational results have also been quite strong. Park’s Q3 earnings showed continued recovery in their urban markets (which were holding the portfolio back), and this if anything appears to have accelerated in October and November. Park recently released an operating update showing the recent strong pickup in YoY RevPar growth.

This growth has been powered by Park’s urban portfolio and also strong performance at their Hawaii assets. This is broadly as I expected – Park’s urban assets should see a nice growth tailwind from increased group & business travel & their Hawaiian assets should see tailwinds from the re-emergence of the Japanese traveler who were ~20% of demand pre-covid but were only at ~5% recently.

I am hopeful this growth can continue into 2024. Park has many large assets that are oriented towards group travel, and 2024 group bookings are trending well above 2023 which should provide a strong boost towards revenue and earnings growth.

Multifamily

Multifamily, fresh off its post covid high, continues to take its lumps. As I discussed in Q3, while demand remains fairly healthy, record high supply levels are driving rental rate declines in many markets, especially those in the sunbelt. See below chart from apartment software provider Realpage.

The minimal prospects for near term income growth combined with much higher rates means the multi market is no longer willing to underwrite the record low cap rates which drove value growth in 2021. Cap rates have been creeping up since 2022, but this last quarter feels like we finally saw many participants accept these higher rates as reality (except of course BREIT who seems to continue to use 2021 marks).

For example, NXRT, a smaller multi REIT, is one of the few multi REITs to publish a regular NAV estimate. And they increased their valuation cap rates by a whopping 50 basis points from Q2 to Q3. I think the increase is fair and was not surprising, but it is nice to see management of a REIT be so transparent about valuation marks.

The REIT market though I believe has over-reacted a bit to the current levels of distress. Again take NXRT – there are some issues here given its external management structure, but historically NXRT has traded relatively close to management’s NAV. Now it is ~$348 vs a mgmt NAV of ~$55. At $34, NXRT, which owns a portfolio of sunbelt B assets, is trading at nearly a 7% implied cap rate. This is far better than anything available in the private markets.

I do think private multi pricing might have some downside risk in 2024 if inflation reignites, as the combination of sustained higher rates + weak income growth could well push cap rates even a bit higher. But if inflation stays subdued I think we are probably near the bottom in private market values, perhaps with a little more decline to come (again ex recession).

That said prices have fallen far enough from the peak to create some distress for those who bought at the top, with value add deals in the sun belt having an especially rough time. We have seen a number of foreclosures in major sunbelt markets and I would expect there are more to come.

Office

The office market continues to be fairly anemic, but critically more and more employers are returning to the office, and some markets are showing the first signs of potential recovery.

NYC – the market I care by far the most about, has seen availability decline a bit from the peak of 16.6% in Q2, and is now around ~16%. The change in itself is hardly anything to write home about, but it is important that it no longer appears to be declining – investors feel far more confident once a bottom has been found than when the knife is still falling. I’d like to see another quarter or two of improvement before officially calling the bottom, but 2 quarters in a row is a good start.

Encouragingly it looks like office attendance in NYC continues to rise. My favorite data providers have not provided recent updates, but we do have real time rail and subway data, which continues to show improvement from when I last shared it 2 months ago. Here is suburban commuter line Metro North data up until mid December (before Christmas).9

Interestingly subway ridership, which has been fairly flat for the last year, also began to show a noticeable uptick post Thanksgiving, moving from low 70s to upper 70s. This is too early to call a trend quite yet but it’s a dataset to watch.

Other markets are also showing some improvement, but the trendline is even more nascent than NYC. DFW and Atlanta both have 1 quarter of vacancy reduction under their belts – far too early to call a trend but better than nothing.

Other markets are having a rougher time, with the tech metros in particular continuing to be especially weak. For example here is the vacancy in San Jose (Silicon Valley) from Costar.

This isn’t terribly surprisingly as the tech majors have not begun to really hire again yet, and have laid off a large number of employees in 2023. Even just recently Spotify laid off a full 17% of its staff.10 Not to mention the impact of many startups and a few larger firms going remote.

There is some hope on the horizon though for the tech markets – money is pouring into the AI/machine learning space, and the pace of innovation has been very rapid. While AI may already seem overhyped in the stock market, the reality is we are just in the first inning in terms of its impact on the physical landscape of the tech markets. OpenAI for example only has ~700 employees! Compare this to Google with nearly 200k employees against a ~1.75T market cap. And thus far almost all of the large AI players are based in the bay area, which may provide a ladder out of this mess for that metro area if they are able to grow and scale up.

Still – WFH’s impact on the tech industry has been significant, and it will take a lot of growth to pull out of the current hole. I do think Silicon Valley will one day again be a landlord’s market, but it is probably 5 years away at least. San Francisco is a different story…

I am frankly still trying to assess the potential overall impact of AI but at a minimum it does look like this technology could power the next wave of tech growth, as there appear to be a lot of areas that generative LLMs can be applied to today. It feels to me like the tech even at its current level (with some polishing) could have large impacts on many large fields such as education, law, accounting, software engineering, marketing/sales, & finance.

As to whether current LLMs are stochastic parrots or actually on the road to true understanding – well I shall leave that discussion for another day.

Industrial

The story in industrial is again fairly similar to what we saw in Q3 and Q2. Fundamentals are the strongest of any asset class, but they are softening as well. Vacancy continues to tick up in the face of heavy supply deliveries across many markets, and is now above pre-covid levels across the US (which were themselves very low levels).

Here is bellwether Prologis’ analysis of vacancy rates and forecast for the next few years.

They have begun to call the current dynamic a ‘mini cycle’, which I suppose is analogous to more of a hiccup than a full blown downturn.

PLD itself though still has a near record 97.5% occupied portfolio, and is still seeing/forecasting rent growth in many markets of 4-6% for 2024. If that figure proves true it would be strong performance relative to what the other asset classes are likely to deliver. If I had to guess, this forecast seems fairly reasonable but I think if the economy enters a recession industrial has more downside risks to demand than other asset classes due to the significant new supply under construction in many markets.

Industrial is in some ways more interesting to me in terms of its comparison to other asset classes. At 4-6% rent growth and slightly rising vacancies, industrial’s near term performance actually would look pretty similar to what I would expect for high quality retail and hotels for 2024. And yet PLD trades at a ~13% premium to Street NAV, which is itself already based on a cap rate in the upper 4s. Compare this to retail and hotels at a discount to NAVs, which are based on cap rates in the 7s and even 8s.

Now the comparison isn’t quite so simple – PLD has a huge embedded rental mark to market which should push their yield closer to 6%, and industrial is lower capex in general, but even after those adjustments I much prefer the retail and hospitality sectors.

This is not so much to say that I view PLD as hugely overvalued, but rather more that I believe retail & hospitality are undervalued.

Speaking of cap rates – they have continued to move up a bit more since Q3. Estimating these is a bit tricky though due to a small number of sales & a wide range of mark to market for rents on individual properties though. I would estimate that similar to other asset classes cap rates should begin to stabilize now that rates have softened up a bit, if inflation remains subdued.

Fin

Overall – the major story in CRE continues to be the interplay of interest rates and operating fundamentals. We have finally begun to see some rate relief, which boosts everything, while operating fundamentals vary widely across asset classes. While rates overshadow everything in the short run, in the long run though what really matters are operating fundamentals and replacement costs. And so in my view the most important thing to remember in this market is that we have seen a huge increase in construction costs in the last several years. Combined with current private market value declines, almost no asset class can justify new construction at current levels (industrial being a notable exception in certain markets). This creates opportunity, as many assets with good demand profiles are still available in the public markets today for well below replacement cost & below current private market values. The private market values will eventually need to rise to levels that will justify new construction, and the discounted REIT values should magnify these gains. The specifics of course matter significantly & vary tremendously, but overall I continue to see interesting opportunities in the REIT space driven by this fundamental imbalance.

Not every asset class or geography mind you, just the big national averages.

That said it would not surprise me if we have a good bit of volatility or further softness in the REIT market in 2024 given how minutely sensitive short term prices appear to be to rates. And I would fully expect some inflation/interest rate volatility in 2024.

USRT is an all REIT index very similar to the MSCI RMZ. I use it in lieu of the RMZ as MSCI charges an insane amount of money for historical RMZ data & as an ETF I can get the USRT data much more easily. The two are typically within ~1% of each other, at least since our inception.

~4.1% today.

Indeed, the job site, just published their latest wage growth data yesterday and it shows continued deceleration in wage gains. At current pace we would be at 2019 growth levels by May. So the above trend wage-growth not looking as likely but we will see what the next few months hold.

Outside of the tech markets that is, and a few covid boom towns.

Sadly he hasn’t posted in the last month or so, hopefully his hiatus is temporary and not permanent.

$31 as of today!

These figures fell over the holiday & have rebounded some but not all the way. The next two weeks of data should be telling here to see if the pre-holiday uptick will be sustained or not.

Even more layoffs have been announced since I wrote this, including Google, Amazon, Discord & Duolingo among others.