War Cap Q2 2024 pt 2

CRE asset class commentary

I am publishing this a bit later than intended, and what a difference several weeks make. REITs in general have done quite well, narrowing some of the performance gap with the broader market. Let’s hope the rest of the year is just as strong.

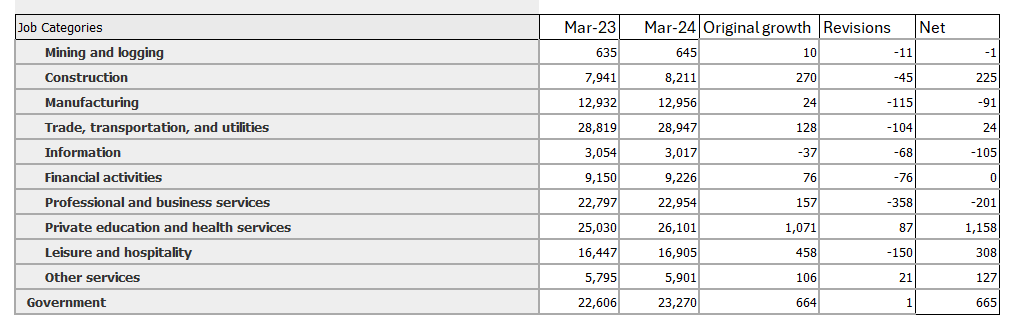

I want to keep this post focused on CRE asset classes, but I do want to note that the continued uptick in unemployment and the downwardly revised jobs figures are quite concerning. I view the employment categories of manufacturing, information, financial services, and professional & business services as the key drivers of the economy, and these have had negative job growth for the past 12 months.

Can healthcare and government really drive the economy forward on their own?

We are at levels of change that are almost always consistent with recession historically. This cycle is anything but normal given the post covid supply driven bullwhip combined with historically low unemployment rates, but the odds of a recession in the next 6-12 months feel high to me, perhaps as bad as 50%. I think we will know one way or another in the next few months whether this is a big growth scare or a true downturn.

Continuing on with CRE asset class commentary, we will begin with retail.

Retail

As relates to our portfolio at least, the biggest story was Macerich’s poor results in Q1 and a meh Q2. This really could be its own post, but the quick summary is that MAC has had some seemingly 1 time issues that impacted NOI, which combined with the new CEO Jackson Hsieh’s plan to let go of underwater assets and potentially sell others to make for a poor first half.1

I do not love some areas of Jackson’s stated plan - especially selling assets to pay down debt. MAC’s debt, while higher for a REIT, is quite reasonable in absolute terms & especially so since their higher cap rates means greater ability to service high interest rates. If Jackson can get good prices I think this is probably value neutral or even accretive (depending on how good the sales are), but if he sells things for poor cap rates (mall liquidity isn’t terribly deep after all), well I’d much rather have the cash flow.

Q2 was better than Q1 but not phenomenal, and overall 24 is shaping up to look weak on overall NOI growth barring a really strong second half. As far as I can tell, the NOI impact seems to be mostly idiosyncratic & timing related, and perhaps some noise from weaker assets.

The reason I remain confident in MAC’s long term NOI growth is that the retail sector continues to perform very well. Across the board REIT management continues to note very strong tenant demand in what is one of the best retail landlord leasing environments in years. The best comp of all for MAC is of course mall giant Simon. Simon continues to report very robust leasing, and also have had strong same store noi growth coming in at 4.5% YTD.2

Now lets look at MAC’s performance. Here is their head of leasing commenting on Q2 leasing results.

A 30% increase over a record year - that is incredible! And yet the market cannot seem to see the forest for the trees. In fairness total leased square footage is trending below 23 levels, but the point remains that leasing is very strong right now, and it is reflected in MAC’s very large signed not open pipeline (SNO).

The risk here is that somehow MAC has a much weaker portfolio than Simon and is going to underperform long term (and that somehow all this leasing doesn’t translate into income because tenants are leaving just as fast as they are coming), but I have reviewed all of MAC’s assets and just don’t believe that to be the case. MAC does have some weaker assets but the core of the business (and vast majority of the value) is very high quality.

Overall I continue to think MAC is a really compelling opportunity. Its combination of high going in yield, low future capex needs, and strong cash flow growth is essentially unmatched elsewhere in CRE.

However for now Mac appears to be very much a ‘show me’ stock, and I suspect they will have to deliver solid NOI growth before being given credit by the market. I don’t know if that will be in one quarter or 4 quarters, but I am confident it will occur.

Retail sales growth also continued nicely in the quarter, underscoring steady consumer demand. Here is the last 12 months of data.3

It is not all roses of course in retail, and there continues to be a shakeout of weaker retailers. A big recent story for CRE is CVS’ plan to close 900 stores. This will of course increase vacancy across the market, but the immediate impact on our portfolio shouldn’t be too significant - drug stores are typically free standing and usually owned more by the net lease REITs than any of the mall or retail REITs. Drug stores are typically hard corners as well, so there should be good demand to backfill most of these spaces.

And CVS is not the only one. Big Lots sounded an alarm recently, and JC Penney continues to struggle, among others. Stepping way back it feels like we are in a period of flux in retail - overall consumer spending is good, but the e-commerce shake out is not quite complete yet. I think there are a number of legacy / older brands which will continue to struggle and perhaps eventually file BK without some kind of real turn around.

This is one reason I prefer malls to big box stores - I think long term the soft goods, luxury goods, entertainment & food profile of a mall tenant base is much better positioned to capture consumer wallet share than legacy retailers who are competing heavily against Amazon - places like Big Lots, Joann’s, Petco, the Container Store etc I think will continue to struggle.

And just look at mall staple Abercrombie’s incredible recent performance. A&F had a blowout Q2 with a whopping 21% YoY sales growth!

While just one tenant, for a long time A&F was synonymous with the mall, and there is a certain symbolic resonance in its recent rise.4

The real key factor here for the retail sector is zero supply growth. What matters for a landlord is demand less supply, and as multifamily shows us it doesn’t matter if demand is really strong if supply is higher still. The reality is retail demand growth is best described as moderate, but paired with zero supply this makes for very nice net demand.

Given the massive escalation in replacement costs we just saw, and higher rates, the rents needed for new development are generally much higher than today’s rents, meaning the retail market generally should have a good deal of room to run before the specter of new supply rears its head.

Industrial

The industrial sector continued to slow down, lead by weakness in Southern California which saw outsized rent growth during the pandemic.

Prologis, always a decent proxy for the national market, revised down its 2024 forecast for absorption from 250mm to 175mm after a very weak Q1. PLD’s Q2 results were better than Q1, but were only in line with their prior guidance cut.

Southern California has had actual negative rent growth - PLD estimates it around negative ~6%, I have seen other estimates from 10 to even 20%. I suspect some of the difference may be in how high some folks marked their top of market rents, and also varies with submarket.

So Cal focused Rexford on the other hand was a bit cagey on market rents in their Q2 call, which is always a bit concerning. I cannot help but be reminded of NYC retail in the mid 2010s by the whole situation. Both markets saw absolutely massive rental rate spikes driven by strong demand and record low vacancies, where deep pocketed tenants bid up prices for the remaining vacancy.5 The problem here is this growth sets the stage for a pullback, as long term rent is not set by what the wealthiest tenants can pay, but by tenants who can pay the least. And this is what we saw in NYC - many investors bought in with dreams of the high rents continuing, but as leases rolled many stores closed as they could not afford the higher rents, and there were not sufficient tenants able to pay the new higher rents. The result was a grueling 5 year period where rents ground steadily lower and vacancy was elevated even in prime locations.

And with SoCal rents up ~100% in a few years, as leases roll and landlords try to mark to market there are going to be a number of these lower end tenants who have to close or relocate, sapping demand. While the long term drivers of SoCal industrial are probably a good bit more robust than NYC retail in the mid teens, I do worry that things could get relatively ugly here for SoCal.

Outside of SoCal, rent growth elsewhere looks to be flat to slightly positive, and some sunbelt markets continue to show decent strength.

Here is PLD on the US markets.

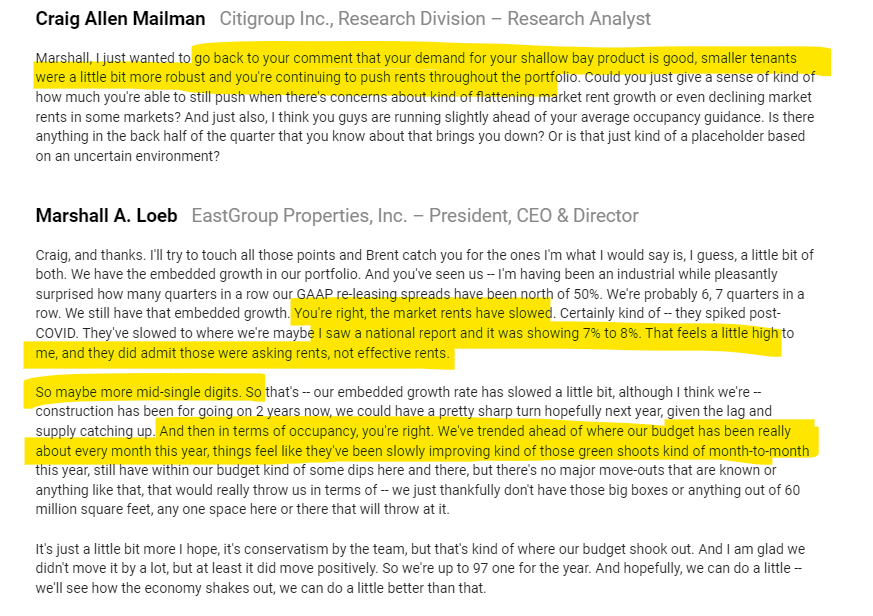

Sunbelt small bay focused Eastgroup is a bit more upbeat, with leasing and occupancy coming in above their original estimates for the year, and market rent growth still coming in positive. The below is from their Q2 earnings call.

So while on a national basis, the combination of significant recent new construction with a weaker leasing environment is dragging down the industrial market, regionally we are seeing a good deal of variation.

Thankfully for owners new construction starts have fallen off a cliff, and so once this wave of supply is leased up (over the next year or two), the market should look much more landlord favorable.

Here are starts in developer friendly DFW as an example - we are essentially at post GFC lows in new construction.

Costar data on construction starts in DFW

Similar to multifamily, investors are aware of this dynamic and have been increasing activity in the industrial space thus far in 2024. This can be seen in a portfolio sale PLD first marketed last fall, took off the market, then brought back this year.

All in all, the covid era industrial boom driven by a rapid rise in e-commerce spending is over, and it looks like the sector should see more normalized growth going forward. As a reminder, e-commerce space takes 3x the warehouse space of traditional retail, so it is a huge driver of industrial demand. While ecommerce’s share of spend has declined from covid highs, I suspect we are not at final equilibrium and there is continued future share growth to come.

But even if growth levels off at the current pace, at a ~25% e-commerce share (I’m rounding here), industrial warehouse demand has essentially been permanently boosted by 50% relative to pre-ecommerce levels given the 3x warehouse intensity of that 25% spend. Combine this with some nascent trends in potential reshoring and the long term demand outlook for industrial still looks fairly sunny once we are past the current rough patch.

Hospitality

Lodging in general has performed fairly well this year operationally, although there is significant dispersion among asset types and geographies. However many REITs have cut guidance on recent consumer weakness, and lodging stock performance has overall been very poor. Outside the macro economy the big story has been and remains to be covid normalization, with a rebound in group and to a lesser degree business travel, and domestic leisure softening from covid era peaks.

This story is almost done, and many markets are pretty close to normal. There appears to still be some recovery to come in the group segment, with hotel firms across the board hailing group as the strongest segment.

Here is Hilton noting they expect modest overall revpar growth, but group is growing at a whopping 10% YoY and is expected to be even higher going forward.

Business, on an occupancy basis is still a little below pre-covid levels, but I still believe we can’t make an apples to apples comparison until tech exits its recent pullback.6

Our largest hospitality investment, Park, had a phenomenal Q1 with Revpar up nearly 8% YoY driven by strong group demand, ongoing urban recovery, and continued strength in Hawaii. Q2 was solid but weaker, coming in at 3.2% revpar growth, with Hawaii beginning to soften a little. As a reminder Park’s hotels are very group oriented, with many big box convention hotels, so Park is very well positioned to ride the ongoing group wave. The other two legs of Park’s stool, urban and Hawaii, both look to have further room to run as well. The west coast markets seem to be picking up, and as I noted in multi they are seeing some quality of life improvements which ought to filter through to the hotel side. Not to mention long term if AI really plays out as a new major sector this should really accrue a lot of value to CA (if pols don’t mess it up) and help many of those markets fully recover.

Finally Hawaii continues to benefit from essentially zero new supply, and still likely has a bit of uplift yet from Japanese travel normalization. In Q1 Japanese air travel to Hawaii rose to 69% of 2019 levels, and while I suspect it won’t fully recover due to the exceptionally weak yen, I would wager we have another 10-15% further recovery there at least. Still - Q2 proved to be soft for Hawaii as US visits were down 2%, and overall revpar was actually down year over year. So while the long term trends look favorable, the shorter run pullback (and shift) in US leisure travel is beginning to take its toll.

Unfortunately hospitality REITs have done quite poorly this year - bellwether Host is down 11%+ ytd as of this writing. Park has performed much better at ~-4.5% ytd, due to its superior group driven performance, but is still a drag on portfolio returns. Softening leisure demand and I believe concerns over a potential recession are what have driven the poor performance of hospitality REITs thus far.

We also made a new hospitality investment in the quarter in Vail Resorts. Besides being near and dear to my heart7, Vail is trading at a very attractive 8%+ cap rate. Given the irreplaceable trophy assets they control8 this is pretty interesting, but the icing on top is Vail’s capex profile. After accounting for typical hospitality type reserves9, Vail has one of the best capex profiles in commercial real estate (after self storage), and that assumes zero ROI on any capex! Of course this shouldn’t be too surprising given Vail faces zero new supply & its primary capital stock consists of long lived assets (lifts).10

I mean who wouldn’t want to invest in this

And that is just the business today - Vail still has a significant opportunity for further growth in the mostly untapped European markets. On the negatives side of the ledger is Vail’s inferior tax treatment due to not being a REIT (although I believe it could become one via an opco/propco split), and earnings volatility tied to weather (which they are trying to reduce via Epic pass sales).

I may share a full write up on Vail some point, but I’ll leave it at this high level summary for now.

Office

The office market, at least at the high end, is showing signs of life. Our holdings here are limited to Vornado, which is obviously only a small very differentiated slice of the market.

VNO had a nice quarter operationally with good leasing, but the real news was the announced sale to Uniqlo of their flagship 5th Ave store for a whopping $330mm. This sale was at a 4.2% cap rate - below the original JV pricing of 4.5%! And it was even lower on a mark to market basis. The market finally has begun to respect VNO’s strong retail portfolio, and the stock saw a big pop after the sale was announced

Some other office REITs have also started to show a bit of momentum in the Q2 figures. In particular sunbelt focused Highwoods and Cousins both had nice leasing quarters, as did all 3 of the NYC REITs.

The NYC market seems to be pretty close to a bottom in terms of vacancy, if not already there. Costar put out a story noting Manhattan actually had a YoY decline in vacancy - the only one of their major markets to show this. Other NYC brokers showed a mix of slight decline, flat and slight increase in vacancy.

Leasing has continued to pickup, although it remains below pre-covid levels (although July and August have been at/above pre-covid levels actually!). But critically the supply picture is significantly improved, and as the last of the pre-covid construction finally delivers net absorption should improve.

And speaking of supply, some big news in NYC office world was the passage of a new law in Albany which is intended to facilitate more office to residential conversions. The law removes a cap on residential FAR the state had set, and also extends a new tax incentive called 485x for conversions which set aside 25% of units as affordable. It is not clear to me if the math on the tax abatement actually works out - I have heard mixed things on that front, mostly negative11. But regardless, this opens the door now for NYC itself to loosen some of the restrictions around office conversions. City planning has proposed a nice set of measures which would allow buildings built before 1991 to be converted, and also dramatically expand the geographies such conversions could occur in12. So the government seems to be movingly slowly but surely in a direction which would support further conversions.

But even without these measures, conversions have begun to ramp up with about 5 million square feet under way or permitted and another ~5 million under active consideration. That is over 2% of inventory right there! The impact of conversions on the NYC office market looks to be significant, as I noted back in my original VNO investment post series (link here ).

Coming back to the demand side in NYC SLG had a great Q2 outperforming its leasing targets and reiterated their belief that occupancy has bottomed and will increase throughout 2024. VNO on the other hand, while it had a good Q2, expects occupancy to hold steady in 2024, and then rebound into 2025 as new leasing takes effect.

Interestingly SLG is raising a $1 billion NYC office debt fund, and the investor reception has apparently been pretty good so far, so much so that at NAREIT SLG indicated they thought they may go over the $1 billion goal.

One more note from SLG’s Nareit presentation - they mentioned demand from tech firms finally coming back.

Names in the market apparently include Amazon, Apple, Inuit and OpenAI.

So we have more signs of green shoots in the NYC office market on the supply front (conversions reducing it), the capital front (increasing investor interest), and the demand front (fairly good leasing, tech coming back into the market).

While NYC is hardly strong, it remains stronger than the rest of the US and I think will be the first office market to become a landlords market again (still a few years out). But pricing may well recover earlier than the fundamentals if the positive momentum becomes clearer, which it seems to be thus far.

Generally I am more bearish on office in the rest of the US & I think things are still getting weaker in many markets. As I have mentioned I think the tech markets may have a ladder out via AI demand, but that is a ways off and there is still more bleeding to come. Slow growth markets are in my view almost untouchable. High quality sunbelt assets seem to be doing pretty well & given a lack of new supply combined with strong population growth I expect that to continue.

Private values are surprisingly strong in a lot of secondary/tertiary markets for lower quality but leased assets – too high in my view. As I mentioned in my last letter, there are some ways to play that relatively strong pricing in the public markets, but I do not like buying into a spread based on what I view as overly high private sector prices. It may work out, but in a downside recession scenario it could look ugly and my primary goal when investing in CRE is to avoid capital loss.

Fin

Thanks for reading - that is it for this update. I’ll be back with Q3 soon, the economic indicators over the next few months should be very telling!

You never really know what is behind a stock’s movements, so this is my best guess. It does seem specific to MAC and Simon is up a good bit YTD while MAC is down, but I could be wrong and it could be something else entirely!

This isn’t an exact comp as nearly half of Simon’s portfolio is outlet and they don’t break out NOI by type, but Simon noted that growth was good across their asset types, so it is probably relatively close.

Some of this is driven by pure population growth and adjusted per capita the numbers look worse. But insofar as retail real estate is concerned total growth is really what matter.

I also used to own some A&F before I decided to focus the fund 100% on CRE as I thought CRE only would be a cleaner story to tell given my background. But considering just about every single one of my non CRE investments has absolutely soared in the last 18 months I’m wondering if this wasn’t a mistake!

Supply was also viewed as being very limited in both markets, which is mostly true but with a big enough price movement some supply will find its way through, which was true of both markets as well.

A spending pullback ex AI that is - obviously stocks are at highs and AI spending is huge, but it feels a little bit like AI is more sucking up all available spending rather than driving a proper boom cycle. To me this is most evident in headcount - big tech has not really begun to hire en masse yet, and I don’t think we will see corporate travel budgets coming back in a big way without more hiring.

Full disclosure, I ski a lot. I usually relocate to the Rockies for much of the winter, and have spent a lot of time at various Vail properties. So I might be a bit biased here.

One critical risk here is that Vail effectively leases most of their assets from the US government under long term special use permits or SUPs. There has never been a cancellation of a permit and I think there would be a popular revolt if the government ever did, but still a small risk nonetheless.

Said reserves are baked into my cap rate calculation as well.

And I would argue that much of their capex does in fact have ROI - upgrading lifts and adding new lifts increases mountain capacity, which allows for more visitors (and therefore revenue) at a given mountain. It is analogous to adding more supply.

To some degree this depends on what kind of future rent increases the rent control board allows, which if I were a developer taking on one of these projects I wouldn’t want to make much of a bet on given how far below inflation recent increases have been and how politicized the process has become.