War Cap Q2 update

An odd market

Apologies for a lack of Q1 – I gave my LPs a brief update but struggled to write a longer letter due to the wild pace of change in Trump’s tariff policies. I would begin writing, then things would change dramatically, and eventually just decided it wasn’t worth the time as I had a lot going on with my private investments1 & actually managing the portfolio.

So now that the macro world has calmed down as has some of the privates work, hopefully we are back to regularly scheduled programming.

Please read the disclaimer HERE - nothing here is investment advice.

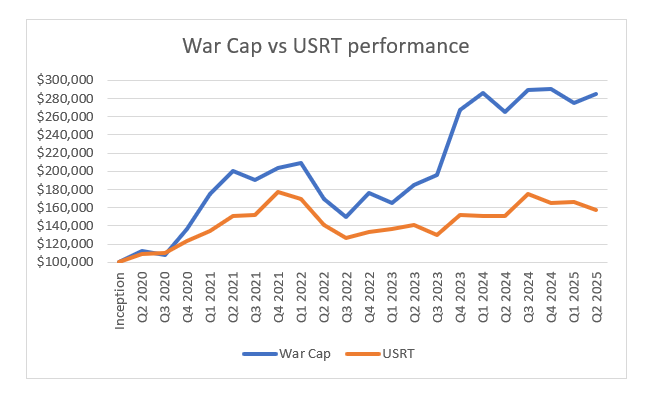

First, the returns as always. We are down slightly at -1.32% for the year, vs 0.19% up for the USRT, and 5.4% for the S&P. We closed the gap significantly YTD with the USRT from Q1, however the S&P gap widened. Nonetheless I remain pleased with our long term outperformance since inception at 186%, vs 57% for the USRT and 130% for the S&P.

While I am not happy we are down for the year, overall I think we had a very nice quarter. We improved significantly from Q1, and had very strong performance against the overall REIT index. More importantly, I feel very good about where our portfolio is today.

The portfolio remains vast majority REIT focused, but I have begun to opportunistically invest in other stocks as I mentioned I would begin to do. In fact one of these other investments, Sportsman's Warehouse, was a strong driver of our performance in the quarter. We invested in SPWH in Q1 and early Q2, at an average basis of $1.68/share - now it trades at ~$3.5 due to strong Q1 results (although very volatile!). The investment here was fairly simple - Sportman’s is a sporting goods & hunting retailer with a large focus on firearms, which has suffered from a covid demand pull forward hangover, over expansion, & mismanagement. Same store sales had been negative for several years now, but a new CEO was brought in and seemed to be making progress turning it around. At our investment price, the stock was dirt cheap if the turnaround was successful - a mere 3x stabilized ebitda (which would itself be well below pre-covid margin and store level sales). The turnaround is certainly not done, but they posted positive same store sales in Q1 for the first time in a long time, and continue to reduce costs and improve margins, triggering a big rally. Critically for me, the category feels like it has real legs, as competitors Dicks and Bass Pro were doing fairly well, and the store base is actually quite new and nice2. The main downside here (thus far) is this was a relatively smaller position, so the overall fund impact isn't enormous. Still - if we have a recession Sportsman’s may be put into a difficult position of seeing sales fall again before their turnaround is complete, so there is real macro risk here beyond the execution risk.

Economic Picture

Big picture, I am still fairly nervous about the economy. I think the markets are being overly sanguine about tariff impacts and also the continued impact of higher interest rates (which has been stretched out due to tariff uncertainty). Hiring is mixed - ADP showed it turning negative last month, and on a 3 month pace is the slowest since covid. However the US BLS jobs data continues to be fairly positive - the one fly in the ointment there is that while the topline numbers are good, the composition is not great. Job growth for the last month was almost entirely government and healthcare, and likely seems reflective of our massive 6%+ of GDP fiscal deficit. However government spending alone cannot power economic growth in the long term.

Critically, the housing market continues to weaken, especially in Texas and Florida, as high prices and high rates push affordability levels to all time lows. Here is a nice chart showing mortgage payments to income from Nick Gerli, who runs a housing data firm. (his twitter handle is @nickgerli1).

When you factor in insurance, which has really risen recently, this is likely even worse.

Aside from government spending, it feels like the only thing keeping the economy running is the AI boom. It is very hard to know if we are in a 1997 type ongoing ramp up, with the biggest surge yet to come, or if we are getting close to the edge. Frankly I feel like we are already seeing some 1999 type levels of froth in firms such as Palantir, Microstrategy and Coreweave3.

On the bright side the tariffs figure appear to have come down from the potential worst case levels, however they will still present economic headwinds it looks like even in a best case scenario. And it very much feels like there is risk here the market is not pricing in - just yesterday Trump announced large tariffs on a whole host of countries, while also extending the self imposed broader deadline to August 1st.

Further in the good news category, inflation itself has actually continued to tick down.

We are basically back to pre-covid levels of inflation, if the current trends continue. The big question of course, is if these trends will in fact continue. We still have very little clarity on where tariffs will shake out, but they are already causing some prices to rise and the impact could potentially be much worse in a worst case scenario.

I do feel like given the Fed’s hawkish stance, inflation will remain low and any tariff driven increase will be a temporary shock. It is painful in the short run, but I think long term will mean it is more likely that we get back to pre-covid levels of inflation (or at least close to that) and thus also lower interest rates. It also probably means a recession of some form is much more likely – potentially something highly regional like we saw in the early or late 90s.

The high rates are causing the sunbelt housing engine to slow, and the next few years might get rough in certain markets. Unsold homes are piling up, and margins are falling for builders.

Construction spending data has also turned negative - this has almost always come with a recession in the post war period, except 1966 when spending turned negative without a downturn.

If the tech boom can endure I would bet on coastal metros to outperform, and techier sunbelt cities to do fairly well (except perhaps in apartments where oversupply endures, at least in some places). If tech also goes belly up, things could get much uglier.4 I think what happens here is highly dependent on progress in AI models - if we continue to see good progress the boom will almost certainly continue. However if things stall out the stage is set for a slowdown there. The current reinforcement learning and model scaffolding vectors feel like they have legs for a bit longer, but cracks are starting to show here as overall model improvement has slowed dramatically and is now more domain limited (albeit to some very large domains like coding). I would wager on this slowing down in the next year, but wouldn’t be that surprised if it went on for longer5.

Hedging

Despite the uncertainty, I feel quite good about our portfolio. Our real estate assets are trading at high yields and significant discounts to private market and historical prices. If/when rates decline, we should be very well positioned to benefit. We have a good deal of cash, and I have also taken out some hedges around the downside risk, specifically focused on what I view as one of the most over-valued stocks in the market, Palantir.

Palantir is a software firm which originally focused on government clients and has since expanded into the private sector. As far as I can tell, Palantir offers more ‘secure’ versions of basic software to clients in government or regulated businesses such as healthcare or finance, and also has a large custom software creation & consulting business. The reason I hedge here is that Palantir itself is very broad and vague as to what it actually does, but the above is my understanding from ground level research.

What is interesting about PLTR is the valuation. Palantir, trading at a wild ~nearly 90 times revenues and 400+ times earnings as of this writing, is by some measures the most expensive large cap stock ever to exist6, and is still one of the most expensive ever when looking across any stock size.

This FT article, which came out a little while after I put the hedges on, covers things nicely. Link here - it features work from a firm Trivariate research who seems to have had much the same idea I did.

Excerpt from the FT piece - it is worth a read in full.

Many of the firms with similar eye-popping valuations historically had huge assets which were not yet generating cash flow (biotechs, LNG terminals, etc). If you strip those out, there are hardly any firms that have ever been this richly valued, and basically every other firm that was has done poorly to horribly over the next several years post peak.

Another way to think about PLTR is, how much would it have to grow to justify the current stock price? A rough heuristic used in the tech world is good software companies trade for 10x revenues. Really good ones can be higher (or during frothy markets). One could argue (and I would argue this!), that this level itself would be much lower during a down market, but lets just assume it is fair for now. MSFT for example is ~13, Google is actually only ~5.5 for some context.

Given PLTR trades at ~90 times sales, what this means PLTR has to literally ~9x their revenues to grow into the current valuation. Lets say PLTR can hold this value for 5 years – to grow into the valuation over 5 years means an annual revenue growth rate of 54%, per year. Over 7 years that number is 36%. Palantir’s own 5 year measure here is a bit over 30%.

Now – is it conceivable that Palantir eventually can grow its revenues from the current $3.6 billion to $32 billion in the next 5-7 years? Certainly. But it would rank among the fastest growth rates at that scale of nearly any firm, ever. And I believe it would be by far the fastest of any software firm of this size.

The biggest revenue growers of all time are products that are consumer oriented, particularly with network effects (Meta, Google, Amazon). This is because the consumer market is the largest market, and network effects can power rapid growth.

The other big bucket of really rapid growth at scale has been cloud services. This is a capital intensive business, but nonetheless is extremely broad in scope as it targets almost any firm. That field has only sped up as it bleeds into general consumer use via AI.

Business software on the other hand, is typically limited to a given market and use, and often has long, difficult sales cycles. And the total value one can charge for the software is limited by the specific value provided and the use case.

A simple example is something like property management software for an apartment complex. Even if you’ve never managed an apartment, likely you have lived in one and can imagine the kind of features software might help with. Tracking rentals, processing paperwork and payments, etc.

So the key issue here is that the software is often very specific. Some components (say signing documents digitally and storing), are obviously common, but others, like tracking tenants and creating a rent roll, are fairly specific to a given use case.

This means the scale of the software is inherently limited by the market it targets. Now one can always add new features (if you can find something users want), or even expand into entirely new markets and products, but fundamentally any given piece of business software is relatively limited in how big its sales can get.

This means business software firms often grow quickly for awhile, as they pick up customers in their initial niche, but eventually slow down as they saturate their given market.

To expand further, they need to build new software products. This is often difficult outside the initial target market.

So fundamentally, business software has just never grown at the rate Palantir needs to growth to justify their valuation, at Palantir’s scale.

Now Palantir makes some very broad claims about what their addressable market is, and who knows, perhaps they really are able to grow at 55% per year for the next 5 years7.

But I’m willing to take the other side of that bet, particularly as a hedge. If we have a recession I will bet that tech multiples are not 10x sales, but closer to 5x or even lower. That would of course compound with belt tightening and slower revenue growth… it wouldn’t be crazy at all to see Palantir trade as low as $10/share in a rough downturn in my view. That would be ~6.6x current revenue, call it 5 with a bit of additional growth.

You can buy puts $40 dollar puts 2.5 years out for ~$4. If we have a bad downturn these could be worth 5x if the stock goes to $20, and 7.5x at 10!8

The beauty of this particular hedge is that not only is the risk/reward skew huge in a downturn, there are a number of non downturn scenarios in which you can get paid as well (albeit likely for higher dollar strike prices, although very possible a $40 gets paid in a 22/23 style tech decline).

There are of course risks here – but as a hedge it is difficult for me to see a scenario where we have a recession and this stock doesn’t come back down to earth. And in a world where it doesn’t I feel fairly good about the rest of my portfolio doing very nicely. The biggest problem with something like this is the fixed nature of the timing with the set 2.5 year window. However in my view that is worth the asymmetric upside achievable, and the fixed downside limit, as compared to a pure short (especially in todays post memestock world). Especially given how wobbly the economy feels right now. So all together I believe the expected value of this investment is very high - but critical to understand there are a good portion of outcomes which are a zero! So these kinds of investments cannot be a large part of a portfolio (unless absolutely uncorrelated).

That is a lot of writing for something that is a relatively small position, but it is a different kind of investment from what I have typically written about so I wanted to cover it in more depth.

Fin

This is starting to run long, so I will again split this into two articles with a second CRE focused piece to come later. There is a lot of news to share there, in general and as relates to some of my investments. If you come here for the real estate commentary, sorry you didn’t get much of that today - you’ll just have to wait for the next article!

As always, thanks for reading.

We just delivered a new self storage facility in Nashville – if you need storage in the area check it out! 2508 Dickerson Pike in east Nashville. It is the first and only facility in the Nashville area with smart locks, which allow for a bunch of cool additional use cases for business and power users. Most notable is 24/7 monitoring of unit access, and also the ability to create access keys with expiration dates. Link here.

Guns and expensive outdoors gear are also both fairly e-commerce resistance categories.

Not to mention the reportedly extremely high pay packages Meta is offering researchers. Zuck going overboard on something seems to be a reasonably good indicator of a bubble - indeed the name change to Meta basically top ticked the 2021 cycle.

Another thing to consider is falling levels of immigration - immigration has driven much of the national population growth over the past several years. It has now fallen off a cliff for obvious reasons, and this is going to bring US population growth way down, potentially to almost zero. This is not great for economic growth, as it could bring population growth negative given low US fertility rates. This is kind of a huge deal and is a trend worth watching if it keeps up.

But I said the same thing a year ago and have been proven incorrect thus far, although my scaling has hit a wall prediction has proven accurate. But I did not appreciate that these other vectors would elicit just as much excitement in the VC world, despite being smaller absolute levels of improvement.

At least in recent memory, I’m wouldn’t be surprised if some of the olden time booms were equally crazy when compared apples to apples.

Most of their clients don’t seem terribly impressed, if you look up online discussions there is almost no one technical speaking highly of the product. And many people I know describe it as more consulting type work.

I like the higher dollar strikes a bit more actually, don’t do as well in a big downturn but more scenarios in which they have a positive EV. But the $40s are a nice example.

palantir is 1/many based on ease of narrative for flipping higher.

no rational analysis possible in golden age of grift.