Q3 CRE commentary

REITs, mountains and more

Welcome to the second part of my Q3 commentary, this time updated with REIT Q3 earnings. Obviously there were some big political changes between this letter and the last given the Trump election victory. I won’t spend too much time on that as I waxed on macro for long enough in the last letter but my general view is this further increases uncertainty. There are potential economic scenarios here which are quite positive (no or limited tariffs, reduced regulation / increased government efficiency), and scenarios which are very negative (significant tariffs, inflation reigniting from potential fiscal stimulus, tariffs, or workforce reduction due to deportations), or some mixture of the above. Given ongoing labor market measure derivatives are showing softness and high market values (along with some things that just feel outright manic or toppy1), I don’t feel like investors are being paid particularly well to assume possible downside risks. But it is hard to predict.

Diving into our CRE asset class specifics, we will start with one of my favorites with retail and malls in particular.

Retail

The mall space overall had an excellent quarter with Simon posting a 5% NOI growth for Q3 (and 4.6% YTD) and 100 bps change in YoY occupancy. This is a strong quarter from Simon, and I believe really validates my mall thesis. Given the robust leasing, we should see several more years of strong income growth from the mall sector overall given large signed not opened pipelines and likely future leasing.

MAC had a more mixed quarter with NOI growth of only 1.8% and a mere .3% change in occupancy YoY. However this didn’t stop MAC’s stock from having an excellent quarter (and now year), seemingly drafting off Simon’s operating strength. MAC is currently around $21/share, and management clearly thinks this is fairly valued since they immediately hit the market with a large share offering of 9% of existing share, for about $400mm in proceeds. This pricing is frankly also right on the nose with my current NAV for the stock.

Why didn’t I just put 100% of my investments in MAC again?

While this offering was at NAV which in theory is neutral, I do not love a big offering like this, as I do think MAC is poised for several years of good income growth and thus likely NAV growth as well. The equity offering thus dilutes that future appreciation, and I don’t see the repayment of already reasonable levels of debt as ultra critical as management seems to.2

Also negatively for me is that it looks like MAC is indeed selling assets at pretty poor prices just to reduce leverage. They appear to have sold the Oak at a 13% cap per their latest earnings call - that is pretty rough. Why sell for such a high cap rate? Occupancy here seems to have been trending in the right direction (90% in 23 vs 88.3% in 22 and 85.8% in 2021), and while I don’t have access to all the same detailed leasing information MAC does it seems hard to believe that this asset is going to fall apart in such a way in the next few years that a 13% cap rate was a good price. Its not the best asset - there is a competitive mall literally across the street, but it doesn’t seem like a 13 cap asset either. Metro LA is dense and wealthy, so generally can support higher levels of retail than elsewhere in the nation.

The Oaks mall

MAC also issued equity earlier to acquire some JV interests at a blended low 7s cap rate. This was a bit dilutive but not a huge deal so I am neutral to marginally positive on it.

Given all of this - MAC is looking pretty fairly valued. It is still a good sized holding for me as I don’t really want to incur the taxable gains and I think it has some room to run, but I have sold some and I wouldn’t be investing as much fresh capital in this stock if I were starting from scratch today or had non taxable capital.

Elsewhere in retail, strip is also performing very well. I haven’t reviewed all of the strip names in depth but using Kimco as a rough barometer (they are the largest strip owner by a good margin), NOI growth is around ~3.25% YTD on ~20 bps of occupancy gain (they are close to all time highs for occupancy). There is a fairly wide range here as there are a number of strip operators.

All this positive earnings momentum is translating into rising investor interest in the asset class. Blackstone for example is beginning to move into the retail world, as seen in their ROIC take private ~$4 billion deal. The value here appears to be a high 5s cap rate, for a west coast oriented grocery focused portfolio3.

Right on the heels of this news, it also became public that BX is buying a ~$200mm soho retail portfolio as well - a bit of a different animal given its NYC, but retail nonetheless. Interestingly BX’s retail buys have all been coastal, as opposed to their sunbelt focused multi strategy.

The ROIC deal is I believe BX’s first major retail deal, and may be a herald of things to come with other large investors moving into the space. If this happens I believe there is certainly room for some cap rate compression on retail given the relatively higher yields here compared to other asset classes.4

Office

New York office, and of greater interest for me, Vornado, both had good quarters. NYC office leasing continues to recover, and is on track to surpass 2019 levels at the current pace, a very positive sign. Even a year ago many found this hard to imagine, but the signs of green shoots were there if you were paying attention & knew where to look.

The biggest news relating to VNO is they backfilled Meta’s space at 770 Broadway with a long term lease with NYU. Details were not disclosed unfortunately beyond an upfront payment of $700mm (sufficient to retire the debt here) & that it is not finalized yet but it sounds like a good outcome.

Combined with the Bloomberg renewal at Alexander’s and it is on track to be a pretty good year for leasing for VNO - if Roth’s predictions are true, potentially the 2nd highest volume in VNO history. This is a bit skewed by the two mega deals at Alexander’s and 770 Broadway, but still!

The other major NY REIT, SLG has also had a very strong year, with nearly 2mm sf of leasing YTD and occupancy rising.

The NYC market is by no means fully recovered, but as per usual the capital markets move well in advance of the fundamentals on the ground. Robust leasing combined with reduced supply (from conversions taking space offline, as I predicted), has gone a long way to rebalancing the market. I originally thought these factors would lead to a landlords market by ~2028, but if the current pace keeps up we may get there much sooner.

VNO was a great investment for me. We bought in the 20s, and doubled down in the mid teens. My fair value was ~$45 at the time. Here we are only a year and a half later, and VNO is within a hair of my original fair value. The supply / demand situation in New York has played out almost exactly as I laid out in my original writing, although demand is probably a bit ahead of my original thinking. On the supply side based on our tracking there are about 8mm square feet of office space slated for conversion (with loans in place or permits pulled), and more in the pipeline. That is ~2% of Manhattan inventory coming off the market, and it could potentially get to 3 or 4% before we are done.

In terms of the rest of the US, the story is pretty similar to Q2. Continued strength in the sunbelt, class A in particular, and weakness pretty much everywhere else. Big tech does seem to continue to shift away from WFH which is net positive for the tech markets, and an additional tailwind, but tech hiring remains pretty limited outside of AI. And the AI funding boom has not translated into much leasing yet, but I do continue to believe AI may be a ladder out of the current morass for SF and Seattle.5

Moving on to the residential world.

Multifamily / Residential.

Overall the last quarter in apartments was pretty dang similar to Q2. Weakness in the sunbelt, and strength (at least relatively), in the coastal markets, with NYC in particular looking good. VRE, which is not quite a clean NYC read through as its northern NJ, but close, had a phenomenal Q3 with ~6.7% YTD NOI growth.6 The most notable development this quarter was some improvements in the coastal laggards, which is to say DC and the tech markets.

There were a few interesting things that happened in the broader resi space in the quarter though in my view.

The first was that Sun (a mobile home park & RV company) had an awful Q3. Sun has 3 main business lines, mobile homes (~45%), and RV & Marina (each also close 20%). US rev guidance was cut 65 bps, to a still strong 4.35%, but a huge cut given 3/4s of the year has already passed! This is interesting - such a cut represents either a big slowdown in the business or a huge corporate miss internally. I’m not sure if it is idiosyncratic or if this is a warning sign to broader economic slowdown - RV & marina spend in particular is fairly discretionary so it will be interesting to see if this is a blip or the start of a trend.

The second is news around Aimco. We were invested in Aimco back in 2022, and we sold when the shares rallied significantly, but I have followed it since then. Recently Aimco’s stock has stagnated a bit relative to other multi REITs, and it is starting to look interesting again especially with some big recent news. Aimco has been marketing two of their parcels in Brickell for sale, with a $650mm asking price that I thought was completely absurd. News has recently broken that Aimco is in talks to sell the property at $500mm (~$415mm to AIV after debt) - still way above my value for this asset. If this holds it could mean a pretty significant slug of additional value to be unlock - the market cap is only $1.2b so the implied sale is a very good chunk of the current equity value.

I don’t love the firm’s capital allocation - they seem to be dead set on doing a load of development in Miami, and recently broke ground on a new development there in spite of weak apartment values. And their track record isn’t great - they are under contract to sell one of their assets, the Hamilton, for $190mm, less than the $194mm they spent on it.7 But on the plus side AIV has stated they intend to distribute the Brickell proceeds to shareholders, which would be great.

And ultimately if this Brickell sale happens the current value is likely too cheap, and I may reinvest in the stock here soon.

Storage

This sector is something I am very invested in on the private side, but do not have any public investments. I do still follow the REITs as proxy’s for market strength, and the story here is generally not great as far as fundamentals go. Rents are down in many markets due to weak demand and significant supply deliveries. And yet developers continue to break ground on new projects, despite an awful operating environment. And the REITs are now trading at slight NAV premiums. It feels a bit like the capital markets are getting ahead of the fundamentals here, but perhaps demand will prove stronger than I expect. New supply is slowing down a bit on average, and if the housing market can stage a recovery then storage fundamentals will hopefully get into a better place.

Industrial

Not much caught my eye in industrial this quarter, it was very similar overall to Q2. Leasing still down YoY but basically inline with Q2. New supply deliveries continue to fall off. And Socal continues to be the weakest market.

The most interesting news I saw in the quarter was a big industrial outdoor storage (IOS) sale from Alterra to Peakstone. This is a sub type of industrial that has gained a lot of traction recently, and is something I have been focused on on the private side. Peakstone was an office focused REIT that has been trying to pivot into industrial, and even after this transaction Peakstone’s IOS exposure won’t be that large as a share of their total portfolio, only around maybe 10%. So the asset class is still not really relevant as a niche in the public markets yet but perhaps Peakstone is able to reinvent itself eventually as an industrial IOS/industrial landlord.

The overall sale was very strong, at a low 5 cap and ~$1.2mm an acre. The portfolio is mostly leased but there is a decent bit of development land as well apparently. There isn’t a ton to do here in the public markets on IOS given how small it is, but it is of interest to me personally given my private investments in the space.

Hotels

Hotels in general have had poor stock performance this year, and Q3 earnings have been mixed overall. In our portfolio in particular Park had a meh quarter, as earnings were hit hard by an ongoing strike at Park’s Hawaii assets, which make up a huge share of PK’s earnings and value. Pre strike Park was on pace to do ~5% ebitda growth, but strike caused a Q3 overall decline of ~2%, with the Hawaii assets down a whopping 18.5% in Q3 YoY!

The strike illustrates why hotels deserve some level of cap rate premia relative to other asset classes, as labor relations present an X factor which could reduce earnings and value, and Park will very likely have elevated labor expense growth at those assets post strike, hurting margins a bit.

Even so despite this I think Park is very cheap, as the strike is just a temporary impact (aside the increased labor costs)8 and their year overall has been otherwise quite good. Park is trading a bit under 9% cap rate today - far too cheap for their asset quality and growth profile.

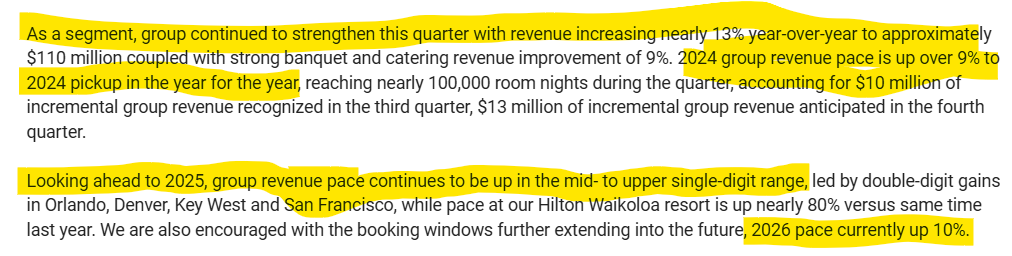

Group pace remains the star of the show, up ~9% YoY, with 25 tracking 6-8% and 26 ~10%.

This bodes very well for Park’s group oriented portfolio!

The story is similar at the operator level - Hilton noted group is driving what growth there was in the US, and that pace was up double digits again for 25 and 26.

So long term I still feel good about our investment in Park, although it has unfortunately been a drag on returns this year.

Vail

Our newest hospitality investment, Vail, had a very interesting quarter and year9. Overall YoY ebitda for 24 declined slightly by ~1% (after adding back a currently money losing European acquisition). Further Vail only guided to a ~2.5% YoY gain for 2025. Revenue for Q1 fiscal 2025 is looking promising, with Epic Pass sales up ~4% (slight user decline + good sized price increase)10. However when we look further into the weeds things start to get really interesting.

The biggest news by far was Vail announcing a targeted $100mm in cost savings! This is against ~835mm in ebitda, so a massive number. This cost savings looks to be generated mostly via by a targeted 14% reduction in headcount, almost entirely at the office level (so not folks on the mountain like lifties). This is a strong level of cost savings if they can pull it off.

The details are that apparently there is a lot of duplication of roles like IT & accounting from resort to resort, and that Vail intends to centralize all of these functions at the corporate level, allowing for apparently some pretty massive savings. This inefficiency is apparently a result of Vail’s huge growth spurt over the last 15 years, having acquired over 35 resorts in that time frame. I am a bit shocked Vail wouldn’t have done these kinds of things all along, but given their strong topline growth during this period, they simply may not have felt any pressure to do so as the Epic Pass & price increases were driving very strong earnings growth.

I am always a bit hesitant about buying management projections at face value, but even half these savings materializing would be huge. At 50% achieved its a ~6% boost to earnings, at 100% its nearly 12%. And they already appear to be making good progress - for last quarter they noted they already had $27mm in cost efficiencies projected for 2025 (partially offset by $15mm onetime costs around severance etc). So $50mm in savings feels like a safe bet, and 100 certainly is possible.

Vail’s Valuation

Vail is trading around a ~8.15% cap rate today (using a 4% capex reserve & .75% bps of current assets for G&A) - at 50% savings that jumps to an 8.6% cap rate. Given the asset quality, historical earnings power & very low capex burden (a mere 12.5% of NOI assuming no capex is accretive, a terribly conservative assumption) that is a strong yield.11

What kind of yield should Vail trade for? On the one hand they do operate leased assets, but these are long term government leases with rents that operate as a % of revenues. I am unaware of any major ski operator losing its lease, although it is always possible.

On the other hand Vail has trophy assets that serve wealthy, non price sensitive consumers, and faces almost no competition from new supply, something that is essentially unique in the CRE world12. Trophy assets are around ~5% cap rates today in several asset classes, so given Vail’s superior supply risk, one could argue Vail ought to be even lower. Indeed Vail’s historical earnings growth is essentially unmatched anywhere in CRE - by my rough calculations pre-covid it was nearly ~13% per year after stripping out acquisitions in the 5 years before covid.

The other risk I’m sure some people would ask about is the climate. Whatever your views on the subject, it is true that the earth has been warming the last few decades, and warm weather one would think is bad for snow.

However the relationship does not appear to be so simple. For resorts in warm areas this does frankly appear to be a big risk, and Vail’s Australian resorts have had a rough time of it recently.

But in Vail’s core operating area (NA), snowfall has not been declining steadily as one might fear. In fact the 22/23 winter was extremely good. The thing is that Vail’s core NA resorts are cold enough that small temperature swings are not massive drivers of snowfall amounts. What matters more is total precipitation, and the relationship with warmth there is much less clear. If anything a warmer world may also be wetter, meaning potentially more snow, at the places cold enough to get it.13 A slightly warmer world may also arguably make skiing more attractive - after all the most popular month to ski is March, in large part because it is warmer! (not to mention spring break making it easy).

So on net I view climate risk as mostly neutral, though there is certainly some level of downside there. The bigger issue here is simply variability - investors hate it, and Vail’s skier traffic is influenced by snowfall amounts. Vail has worked to minimize this with their Epic pass being sold in advance, but weather still has an impact and arguably is one reason the last year was relatively weak, because the 22/23 season was just so strong in contrast.

All this said - I view a 6% cap rate as a very reasonable estimation of value for Vail (~75-100 bps above other trophy type assets for a nice margin of safety), which would put the stock price at more like ~$280 / share. And that is before any potential cost savings, which even at 50%, combined with ~4% / year earnings growth (vs 13% pre covid!), and you could see the stock at ~$350 in just a few years.

And that is just a base case scenario whereby Vail is able to grow earnings at +-4%/year going forward. There is reason to believe this could potentially be much higher.

Vail Upside

Vail has two big potential areas to outperform and continue to drive really strong earnings growth over the next several years. The first is the simplest, and that is ski pass pricing. Vail’s epic pass is currently $982 for the year. It was in fact $979 in 2021, and $933 in 2020 before the recent bout of inflation. Vail dropped the price significantly in 2022 to drive unit growth and have been raising it back since.

If you apply a simple 30% increase from the 2020 price to account for inflation, this would yield a price of $1,220, ~24% higher than today. Further the only other multi resort ski pass out there, the Ikon Pass, which offers fewer resorts, costs $1,449 for their primary pass with no blackout dates14, even higher still! Ikon offers a cheaper version for $1,019 with fewer resorts, fewer days at certain resorts, and blackout dates. Vail has a similar offering called the local pass for $730/year.

So based on Ikon’s pricing and simple inflation, I think there is an argument to be made Vail could push the Epic pass price cost significantly over the next few years (potentially ~30%+), which could really boost earnings.

The other big area of potential upside for Vail is Europe. Vail recently acquired two European resorts, and is essentially trying to take their American roll up playbook to Europe. Europe is a much larger ski market than the US - I’m not sure how high quality this data is but it looks like Europe has ~30mm skiers vs ~18mm in the US. The difference is also really visible in the number of resorts - there are tons of ski resorts in Europe - primarily the Alps but also Scandinavia, Pyrenees, Balkans, Russia & Carpathians. Again data is a bit fuzzy (especially I suspect relating to exact definition of a resort), but in America there are maybe ~480 resorts it seems, vs seeming 2k or even as high as 4k in Europe.

The strategy is pretty simple - buy resorts at reasonable ebitda multiples, then drive scale efficiencies on revenue (with pass sales), and costs. Frankly I do not know if this is going to work in Europe - the market is very different than the US. I love skiing in Europe and it is hard for me to see the Vail model working really well there honestly. Europe is far less corporate, and has a much better food and apres ski scene - basically the opposite of Vail. But it would be foolish to give this no chance of working - Vail may be able to learn some things from its European resorts and create a new operations model for the continent.15

To recap - Vail is a collection of irreplaceable trophy assets almost completely insulated from new supply pressure trading at over an 8% cap rate, which has multiple potential levers to pull to significantly increase earnings over the next few years. As a skier am I biased here? Almost certainly. But I still believe there is nothing else quite so attractive anywhere else in the CRE world.

Fin

Including but not limited to - permabear Rosenberg capitulating (kind of), Masa Son announcing a $100 billion investment, the madness around MSTR and its now copy cats (and crypto in general), and let us not forget Blackrock basically saying the business cycle is over.

In fairness I think Jackson is just responding to conventional sell side wisdom for low leverage levels on REITs. His background is on the sell side as a RE banker so this makes sense.

I have seen others like GS say 6.2% cap, but I’m getting more like ~5.8% ex one redevelopment asset, which I’m unsure of the value of.

Some of this is due to higher capex loads, but arguably much of that high capex was the result of extended operating weakness which required operators to undertake significant re-positionings to attract tenants and reconfigure spaces. Retail has the potential to be an extremely low capex asset class, as tenants rarely leave if they are doing well, unlike office or industrial, and renewal TI costs are typically low. So in a world where tenants are doing well (and thus renew), LL capex is much much lower. This has not been the case the last 20 years, but that appears to be changing now.

But perhaps not! Thus far one of the best uses for AI appears to be assisting in coding, so conceivably a scenario which plays out is AI firms grow but this is offset by firing or a lack of growth in legacy tech firms as they are able to increase their engineering efficiency significantly.

Some of this is also may be a function of a changing same store pool as VRE moved a new development into same store recently and it is unclear if they left in a bit of lease up in before the move to juice SS results.

This is on top of a whole bunch of random side investments which have had a pretty varied track record. The oddest was an investment in a life sciences developer - a sector not doing so hot these days.

One could argue strikes and the associated disruption + higher wage costs are a ‘recurring non recurring’ item, happened sometimes at the end of a labor cycle. I do feel like these though are more one time, given the huge inflation bout we experienced which required significant renegotiation of all multi year fixed contracts like unions have.

Or I should say quarters as we also just got their fiscal Q1. Vail reports on a different cycle than most firms.

Vail generates a huge share of its revenues from annual ski pass sales, called the Epic Pass - over 35%. If you are a skier you have probably heard of this and may even have one yourself. These passes are sold in advance of the ski season, and purchases end on December 2. The idea behind this was to get skiers to commit to paying for tickets in advance of the season, and thus reduce weather based variability and make revenue more recurring / sticky. Thus, by December, there is good visibility into revenue for the following year as passes are locked in. The other 2/3s though, which consists mostly of lift tickets, ski school, dining, & retail/rental, is going to run more variable with skier visits.

A sidebar on capex - 12.5% would put Vail at one of the lowest capex burdens in the CRE universe. Self storage is typically regarded as one of the best and they are around ~8%. If you assume even a little bit of Vail’s capex is accretive (while I fully believe it is - building new lifts and restaurants increases revenues), Vail could easily be at that same level of capex burden.

While it is possible to build a ski resort, practically speaking it is extremely difficult as the government owns much of the relevant land, and isn’t keen on developing park land. Further local opposition is fierce. So how hard is it? Well the Mayflower, the only major ski resort to deliver in 40 years is just coming online at Deer Valley. The developer of this project had to use a loophole with the Army to get this approved (its technically an army resort and they set aside a certain percent of rooms and passes for veterans) and it still took 10 years. It is also extremely expensive - the full cost of Mayflower is estimated at $2 billion vs ~$10B EV for Vail currently. There is an argument to be made here for buying at a discount to replacement cost as well - at that kind of cost Vail’s core western resorts could be easily $15 billion to replace, perhaps even 20 and you are almost certainly over 20 on a whole portfolio basis. The comparison is a bit apples and oranges - Mayflower obviously is brand new while some of Vail’s facilities are older. But Mayflower's terrain is also pretty poor (a southern aspect means lots of direct sun and thus poor snow quality), while almost all the core Vail resorts have excellent aspects and terrain. The final note here on supply is the market is clearly so under supplied in my view that I don’t think Mayflower will have much impact on Vail’s Park City operations. If you’ve ever been skiing on a weekend at Park City it is basically filled to capacity, and there are frankly lots of people who don’t even go on a weekend because it is so crowded. If some folks switch to Mayflower there are plenty of others to backfill.

This is all a bit simplified and dryer / colder climates do drive higher snowfall to precipitation ratios, but I will refrain from nerding out on snowfall here. Also Vail can of course also invest in snowmaking operations to compensate for poor snowfall, which they have been doing.

Blackout dates are where you can’t ski on certain busy weekends or holidays.

There is also some chance this could drive increased efficiencies in the US. European mountains (and Japanese for that matter) have FAR less on mountain staff than US mountains do, and if Vail can take some of those efficiencies and import them back to the states it could be huge. In particular European lifts typically have just 1 person in the booth running it, while the US often has 2 people per lift. Also Europe has way less ski patrol than America - this one may be harder to import due to the US’s trigger happy lawsuit culture though.

Another potential area of imported improvement would be in food / apres. The food at Vail’s mountains is frankly terrible, and apres is non existent at many of them. If Vail could import some of the euro vibe to the US I think it could be a huge success. And Whistler is already somewhat like this so there is some Americas precedent.

Great letter, as usual! Thank you very much.