Musings on Millrose Properties

A rough start for the first public landbank

I took a look at Lennar’s land bank spinoff, Millrose Properties (MRP) and thought I would share my thoughts. The whole structure is just fascinating, and the S-1 feels like it was designed to obfuscate the underlying fundamental truths here, which in my view are pretty ugly.

First though as usual - nothing here is investment advice. Please read my full disclaimer here.

As a quick refresher, a land bank is an entity, usually associated with a homebuilder, which owns the homebuilder’s land inventory. There is a pretty wide range of structures here as far as I am aware, from wholly owned subs on balance sheet to off balance sheet with outside capital. The general point of a land bank is to segment off the land development component of home building, which is capital intensive and can take several years, from the home building piece, which while also capital intensive is much quicker, often taking only 4-5 months. This is generally part of an attempt to convince the market to treat a builder as more akin to a manufacturer than a real estate development business.

Lennar used to have most of their properties on balance sheet, but they recently spun off their land portfolio into a publicly traded entity called Millrose Properties. It sounds simple enough, but the structuring here is actually fairly complex and kind of crazy (and interesting) in my view.

The first thing I found interesting / odd is that Millrose is structured as a REIT, with regular dividends. Homebuilders are precluded from being REITs because they turn over their assets too quickly to comply with REIT rules. Now I’m no real estate attorney but Millrose / Lennar seem to have opted to use a very interesting and unusual strategy to work around this - they created a $4.7 billion dollar loan from the sub which holds the land to the REIT mothership at a 7.5% interest rate. REITS are allowed to hold mortgages (indeed there are loads of mortgage REITs), and so it looks like Millrose has taken the position (and presumably some regulator blessed it) that the mortgage ‘cleanses’ the bad home sale income and makes it REIT compatible.

The legal structure of how Millrose is actually paid by Lennar whereby they get monthly option payments and the land sale is just return of capital (more on this in a moment) may also contribute to making this legally OK - said structure is also very interesting and frankly not a great deal for MRP.

Lennar obviously wasn’t going to spin off their land bank without having some influence and control over the land going forward, but still the structure is really something else.

Essentially what Lennar has done is given themselves permanent 80-90% LTC financing for their land development at a 7-10% interest rate (starting at 8.5% today), in perpetuity, at terms far more generous than any lender would ever give. It’s a phenomenal set up for Lennar and an awful one for MRP shareholders.

Let me explain. Essentially what happens is this - Lennar contributes a 5% deposit based on total cost (land + horizontal development costs, so roads, utilities etc) for the right to an exclusive option to purchase finished homesites. Lennar must pay a second 5% deposit either at termination or, oddly, seemingly at MRP’s option based on MRP cash needs1. For simplicity of analysis, we can assume land and horizontal costs are 50/50 (in high end markets land is higher, cheaper horizontal is higher), and that the deposit is paid up front. This translates into what is essentially a 10-20% equity payment by Lennar for the control of the land parcel. Millrose in turn funds the land acquisition costs and the horizontal development costs.

The equity analogy is imprecise but close enough for a rough understanding as this is the capital Lennar has at risk of a loss. If Lennar were to walk from the option before any horizontal work is done, the loss is 10% (in our 50/50 value scenario). If they walk after everything is done, it would be more like 20%.

What Millrose receives in return is a fixed monthly payment, basically like interest on a loan. It is fixed at the time of each deal, based on a spread, but within a range of 7-10%. Critically, MRP receives zero upside from any land value appreciation - they must sell the finished lots to Lennar at cost!

Another thing that is crazy is that Millrose essentially has to accept any deal Lennar brings to them (presumably assuming MRP has enough capital, though I’m not 100% on that), so MRP is basically a captive entity.

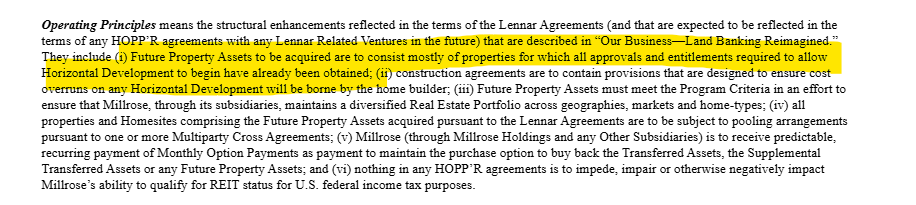

There is even more ugly structuring here. This bit is somewhat unclear to me, but it looks like there are no clear guardrails on the price MRP pays for the land in the first place, nor how exactly the initial entitlements process is handled.

MRP can own land that isn’t entitled, but they heavily advertise that most of their land has no entitlement risk and that they don’t intend to take much of this on.

Mostly is quite vague & broad.

However from my quick review of the relevant agreements, I can’t find anything actually limiting how much unentitled land MRP can own.

And the problem is, all new land needs to be entitled. This process (procuring correct zoning and utility approvals) takes a long time, costs a fair bit of money, incurs some risk, and most importantly can create a huge amount of value. So this begs the question, how will the pipeline be refilled? Lennar seemingly controls the entire entitlement process, and as far as I can tell can bring a deal to MRP when Lennar wants. This creates a host of potential issues for conflict, to the benefit of Lennar and detriment of MRP.

The biggest issue is that Lennar could bring an unentitled parcel to MRP, and have MRP buy it at is unentitled value. Since MRP’s deal with Lennar is at cost, this means Lennar gets to effectively buy the finished homesites at the unentitled value, without assuming any of the entitlement risk!

As an aside if you are not aware, the price of unentitled land vs entitled land is often dramatically different, depending on how difficult entitlements were to achieve etc.

That is all pretty bad for MRP, but I have saved the very best for last. Lennar has a unilateral right to halve payments to MRP for 6 months (they call this a ‘pause period’), something they can do twice, with no penalties or cost! On top of that Lennar has what seems to be a permanent right to implement additional pause periods whenever Lennar wants, and the only cost appears to be a loss of their fixed rates of return (eg presumably the parties would have to negotiate a new rate so this would free MRP a bit, but there are so many other hooks in the docs I feel like this wouldn’t mean much).

Oh and as a cherry on top, MRP is paying a hefty management fee of 1.25% of assets to an external manager, Kennedy Land, for what appears to be basically just rubberstamping Lennar’s deals.

So there we have it. A permanent, ~85% LTC lending facility for land development from a captive entity at 7-10% interest with a right to halve interest payments essentially whenever Lennar wants! Incredible.

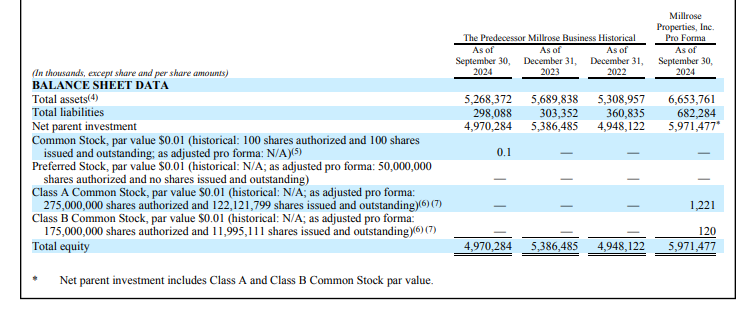

Are there any positives here for MRP shareholders? The one saving grace is that the firm is trading at a decent discount to the book value of its assets. As of this writing MRP is trading at ~$4.4 billion vs ~$6.6 billion of assets (the liabilities seem to just be Lennar deposits which MRP gets to keep in most scenarios so we can ignore them).

The ~6.6b in assets yields ~8.5% gross, or closer to 12.75% gross against the current $4.4 b in value, or ~11% net after management fees and likely other expenses. On an absolute basis that seems OK, but this is for what is essentially a land loan. Land, for those who do not know, is basically the most volatile part of the real estate market, as its the plug between value and cost. If land is ~10% of value of a home, and home prices decline 10%, guess what? The land is basically worthless2. Across the US the rule of thumb is land comprises ~20% of a final home’s sale price. In affluent supply constrained markets that can be much higher, in rural areas even lower.

If you own the asset, that can be OK as your downside risk is counterbalanced by significant potential upside as well. The problem is a lender has no claim on the upside, but is fully exposed on the downside. Lenders are aware of this dynamic and as such do not like making land loans, typically they require low LTCs, high interest rates, or usually both.

Lennar is also aware of this, and so it looks like they created this interesting beast to circumvent the lending market entirely. Now the cost wasn’t free - Lennar lost ~$2.2 billion on the spin in theory based on current stock price. However I suspect that management believes that A) their land holdings weren’t being appropriately reflected in their market cap anyways (this is extremely common in public RE), B) offloading the land to a captive entity will allow for increased margins and profits, & C) this will also allow more consistent earnings and potentially increase Lennar’s multiple, or some combination of the 3.

MRP being public also gives more advantages - now if Lennar wants to expand, they can do so on MRP’s dime using the equity markets. MRP is already looking at ways to raise additional capital (all of which would be bad for shareholders, either raising equity below book value, thus dilutive, or levering up what is essentially already a highly levered company).

In fairness MRP is trying to expand outside of the Lennar relationship, which would be good if they can get better terms but if they are just offering the same deal to other builders this is just more of the same awfulness.

Fin

Overall - a structurally flawed entity on many levels, and the current pricing doesn’t feel cheap enough to ignore the flaws. The discount is decent sized though and the dividend yield is relatively high, so I can’t bring myself to short the stock, but this certainly isn’t something I will be investing in at current prices. Usually when I find a bad deal I stop far earlier in my research, but this company was so unique and interesting I couldn’t help myself but dig in a bit more & so thought I would share what I saw.

This is strange as MRP would obviously want to get the cash up front but there must be something buried in the docs governing when they can call it specifically.

It is not quite this simple - landowners obviously wouldn’t sell for nothing and also know the value will likely eventually go back up, so in practice they just don’t sell. So functionally what happens is land sales freeze up until prices recover enough to give the land a bit of value. Buyers also obviously understand the option value of land, so that helps support pricing somewhat as well.

Fantastic. Loved your YAVP appearance & insightful background here.